Mutual credit in Colombia: Mercedes Bidart of Quipu Markets

Today I’m talking with Mercedes Bidart, of Quipu Markets. Mercedes, you’re from Argentina, the project was born at Massachusetts Institute of Technology, where you did a Masters; and the project is being launched in Colombia. So it’s a very pan-American project.

I saw an article about you in Forbes magazine – I’ll put a link in the description. So before we talk about the details of the project, I want to talk about what drives you. What’s the problem you want to help solve with your work?

I’m an urban planner, so I’m driven by cities, and how they work. What I’m upset about is that we accept as given that one in four people, at least in Latin America, and in the world, one in three, live in informal settlements – in these places that we walk by as if they’re okay, but in fact, I think these places are just left behind. They lack access to proper infrastructure – housing, water, sanitation. But at the same time, they have really vibrant economies, that are vital to the operation of cities, but they’re not able to retain wealth locally. So there’s a problem. How could these economies work better for the people in them? So that’s what I’m passionate about – how we close the gap between those who make the economy work, and those who benefit from it.

How does what you do address that problem?

Well, I hope my work addresses the problem. It’s such a big structural problem.

We have to start somewhere.

Right. The way we face this problem is to ask ‘how we can create alternative economic systems that work for the people who do the work? ‘.The question for us was ‘how can technology foster a more collaborative economy?’. So we started a process of co-design of technology – a digital platform – with people living in these neighbourhoods. This is how we came up with Quipu, a platform that:

- visualises commerce between micro-businesses in informal settlements

- gives them a trading system that allows them to trade without using money

- records their transactions so that they can build a credit history for the first time – which could give them access to better financial services.

That’s what we’re doing, in a nutshell. The 3 main problems we’ve seen are lack of visibility of the businesses – who’s selling what, and where; then a lack of liquidity – there’s not enough money to trade; then a lack of access to capital – any access to capital is extremely predatory. So it’s all about how we can create and retain wealth for our communities. I’m sure you’re seeing this in the UK now – but in these places it’s structural, and it’s always the same, not just in times of crisis.

Yes. Someone said to me recently that soon, there’s not going to be much money at all in UK communities. I said that that’s been the situation in most of the world for a long time.

Yes. We call it an emergency on top of an emergency. Poverty and ‘informality’ is increasing, but the problem was there before.

So tell me about Quipu Markets. It’s a digital marketplace where informal businesses can trade with each other more easily, without money?

Yeah. We call it a community digital marketplace. The community part is important because it mirrors the traditions of informal commerce. It’s tailored for proximity, and the practices that happen in these hyper-local economies. Businesses that upload their products and services can trade with one another using mutual credit or pesos.

And the tokens are digital?

Yes. But the pesos are not. Having some cash in their hands is very important for people. In the co-design process, the traders said that the platform could be a solution for them, but at the same time, they need some pesos to buy things from outside the community.

How many businesses were in the co-design process?

This is called participatory action research, where the beneficiaries of the research are actually the researchers. We trained micro-business owners living in public housing in an informal community in Colombia as researchers, and with them, we designed the questions, carried out the research and analysed the results together. We call it production and consumption mapping. We built on the experience of Grassroots Economics, doing similar things in Kenya, and Banco Palmas in Brazil, but we actually trained the beneficiaries to do it.

After this, we just started drawing solutions – what a community platform would look like. This took one-and-a-half years – a lot of community work, working out the features, and how it could work for users.

And it can be used on phones.

Yes. It’s a web-based platform. Access to smartphones is there. More than 70% penetration in Colombia – more than 3 times the African level. But the phones are usually good enough for apps, so we went for a web-based app.

So the businesses go onto the platform, where they can be found, and you can trade with them on the platform?

Yes. So if I’m a business owner, I create a profile. I validate my profile by uploading a photo of my ID and a selfie. Then I can fill out my details, including my products and services. Your profile is then validated and you are allocated a certain amount of tokens, with which you can start trading. There’s also gamification. The more you trade, you get certain rewards and stars. We’re saying that we’re changing the rules of the game, so that if you spend more in the community, you get better scores.

So when your business joins the directory, how many tokens do you get?

30,000 pesos, which is around $20. Low amounts, but prices in the communities are very low. 30k pesos is usually enough for around 3 purchases. But to ‘unlock’ the third purchase, you need to sell something first. This is our first experiment. We’ll see how it works, and we can adjust as we go on.

Can you do a single trade in a mixture of tokens and pesos?

Yes. So imagine I’m a business owner and I make cakes. If my cakes are $10, they will be $10 on the platform, but I can say how much of this I will accept in tokens. So maybe I will accept $5, or 50%, in tokens.

Could you accept 100% in tokens?

Yes. We encourage business owners to do that. But sometimes it’s not possible, for example if you have to buy things from outside the community for your business.

So you could pay the tokens on the platform, and then when you go to collect the goods or services, you pay the rest in cash, face-to-face?

Exactly. But we’re letting transactions happen between the users. We don’t facilitate the delivery etc. – just the trade.

Do a lot of the businesses have no official premises – they just trade in the street, or from home?

All of them – from their homes. We’re in our first pilot, in a community of 10,000 people in a town on the Caribbean coast of Colombia, they live in public housing, and all the buildings look the same. When they developed the neighbourhood, they didn’t leave space for economic activity. Most people moved to these kinds of places because of the armed conflict in Colombia. They have been displaced from where they were living. Maybe they had been trading from home in their previous communities, and so now they’re transforming their homes into businesses. So maybe they’ll knock down a wall, add a canopy and open a restaurant. But they live there too. That’s how these hyper-local economies work. So rather than calling it an informal economy, we like to call it the popular economy – because informal sounds as though it might be illegal. And actually, it’s how about half the economy of Latin America works this way.

And how many markets do you have – in how many communities?

Just one at the moment, in Barranquilla. But we’ll have different markets in different communities. In as many communities as needed. The pilots are being funded by the IDB – the Inter-American Development Bank. The idea is to use the same platform, with necessary adjustments, in as many communities as possible, starting in Colombia.

How long has this first market been running?

We started three weeks ago. We had some trials before, but this was the official launch. We had a big social media campaign, with videos. What’s impressive I think is that it was an entirely digital campaign, because of the lockdown – and we got 200 users in a week. There was a lot of interest. Now we’re working with those businesses, helping them to finish their profiles etc.

That’s really encouraging.

It is.

So did you have to find lots of trading loops in the community before you could launch it? Did you get commitments from businesses to trade with each other?

Yes. The key was working with the 40 co-design businesses – ‘champions’ we call them. They’re real champions. Even though we weren’t there in person, they were able to spread the word and recruit micro-businesses. Now it’s a network of people helping each other.

Have there been many trades?

Not as many as we’d like. It’s a process of trusting the system, especially that there won’t be any mistakes. So now we’re looking to increase transactions. So far we’ve had 25+ transactions. So that’s our priority. How to explain a totally new system – going from the cash base to a mix of cash and credits. But we’re learning.

How are you reaching out? What’s the most successful technique to get people to join?

For the soft launch, it was word of mouth. But that wasn’t as effective as the digital social media campaign. We also put posters up in the community, with the web address, and people signed up by themselves after watching the videos on the website.

Do you employ brokers, to encourage people to trade?

It’s tricky. We started working with the champions, as I said. There are now a few people actively encouraging people to jump in and trade. But it’s not a paid job. They just have leadership in the community.

What different kinds of businesses are involved?

I’ll try to share the screen.

[Mercedes shares the screen – see video, from 24.15.]

So here’s the marketplace, and you can see that there are barber shops, painters and decorators, home schooling, construction, lots of food providers, so you can find everything you need. What’s interesting is that new businesses started. For example, this one, offering security for people’s homes when they’re not there. This business didn’t exist before the marketplace started. He saw that he could offer something now that his business could be found. You can see that he offers the service for 6000 pesos per hour, and he will take 50% in tokens. Plus he has an offer at the moment – 10% discount.

[Mercedes shows how to transact a trade.]

I can start a chat with him too, about how he’s going to deliver his service. Or, I can add his business to my ‘wish list’.

That’s a really nice looking platform.

Thank you. It’s down to the co-design.

You used the term mutual credit. So you consider yourselves a mutual credit scheme?

Yes.

So we’re starting mutual credit clubs in the UK, and there will be federation software that will allow businesses in different clubs to trade with each other. Will that be the case with you in Colombia, and do you also want to start markets in other countries as well?

We’ve received interest from a lot of places. The situation is the same in Argentina, Brazil, Ecuador. We’re analysing the opportunity costs of operating in new countries. At this point we’re very focused on Colombia but we’re open to looking at opportunities in other countries. Regarding the trading between communities, for now we see that each community will be separate, but at some point that’s something we want to develop – or we could connect with your solution.

Let’s talk later – that would be great. Why not link mutual credit schemes all over the world. Let’s try to build a new kind of economy.

That would be amazing.

And I heard that you visited Will Ruddick and Grassroots Economics in Kenya. How was that?

It was great. That was right at the beginning of my research. I spent a month in Kenya, doing 2 things. The first was financial inclusion workshops, where we were designing all sorts of financial technologies with people living in rural areas, close to Nairobi. After that I really wanted to visit Will, to see with my own eyes what was going on there. So I went to slum communities in Nairobi and Mombasa, and actually I was there the day they launched their blockchain wallet. It was a busy day for Will and his team. It was very interesting to see the similarities and the differences with Latin America. The informal settlements are similar in many ways, but there are critical differences, like the way that people use their phone. In Africa they use a lot of ‘dumb phones’ (which is what they call them, because they’re not smartphones. In Latin America, everyone has a smartphone. But they are used to mobile money in Kenya more than in Colombia.

Does it work in the same way as Quipu?

I don’t know exactly what they’re doing over there now. I know they’ve changed the way they issue the currency. So I don’t want to say in case I’m not up to date.

I’d like to interview him. I think I need to do some homework first to discover exactly how it works in Kenya. It sounds more complicated.

It is. We spent a lot of time talking about different things. At the time they were working on a protocol for currencies to exchange from one community to another. So that’s similar to what you’re doing in the UK. But I’m not sure if they’re still working on the same thing.

So what’s your ambition? What’s the plan?

Well, we envisage a world where the economy is owned by the community. We believe that communities can design their own economies. So that’s our goal – to help as many communities as possible to design their own economic systems. We just provide a tool. We know that technology won’t solve everything, but we’d like to see a world in which the economy is more just, more democratic, in the hands of workers, and we envisage a world where we can design more technologies like Quipu, that are tailored for how workers and communities work.

That’s music to my ears. And I guess that if you’re really successful, those low-income communities won’t be low-income any more?

If we’re really successful, yes. The problem is systemic. As communities I’d like us to be aware that it’s a systemic problem. I take this from one of my mentors at MIT, Otto Scharmer, the creator of Theory U. He says that we need to enable communities to see and sense themselves – how we can see and sense our own system, so that we can transform it. That speaks to how we relate to one another – in a more collaborative, solidarity way. So with tech, we can help to spark something like that. That would be our ideal.

That’s our outlook too. I’ve spoken with people in working-class communities in the UK, and they say that there’s not going to be very much money around soon, and I take 20 seconds to explain what mutual credit could do in a community with no money – that people can trade with numbers in an account, without needing money. And they get it. So this could be a good thing that’s come out of COVID, as well as all the bad things.

100%. It’s a moment. We’ve been waiting for a moment to be able to explain how we could build a new economy. A term Otto uses is ‘awareness-based system change’ – how we can change systems by being aware of them, and how they could change.

I know you’ve spoken with Dil before, and the mutual credit clubs idea was his. He’s written an article called the ‘Transcender Manifesto’, in which he says that we’ll bring about real change not by voting for a particular political party, not by trying to overthrow the system, but by transcending. We’ll just build from communities, grow and transcend.

I agree.

Just finally, the name of your project. I looked up quipu, and it’s an Inca calculating machine, like an abacus, but with knotted string.

Exactly. The story is great. They’re like necklaces with knots. Our logo is a digital quipu. It was also the written language for the Incas. They didn’t have writing – they used quipus. Not just for numbers, but also for narratives. They were recording stories with knotted string. Researchers have understood the number quipus, but they can’t understand the narrative quipus. When the Spanish came, they saw the way they were communicating with each other, in ways they couldn’t understand, and so they burned them all. So for us, it’s coming back to the roots of trading, but with technology.

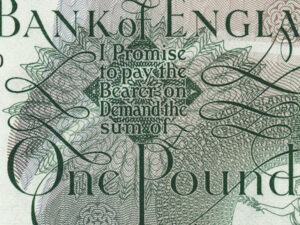

We have something similar in the UK. Historically, we had something called tally sticks. You take a stick from a tree, make notches to record things like how much tax someone owes, then the stick is split in two, with both parties keeping half. So they can be put back together and changed – but you can’t cheat, because if you try to change one half, you can see that it’s been changed when you put them back together.

Mercedes – I wish you all the best. I’m sure you’re going to be successful, and I’m also sure that we’re going to talk again, about merging our projects to build a new kind of economy.

For sure. It’s great to be connected with you. Please keep me updated, and I’ll do the same.

Highlights

- What I’m passionate about is how we close the gap between those who make the economy work, and those who benefit from it.

- Businesses that upload their products and services can trade with one another using mutual credit or pesos.

- The key was working with the 40 co-design businesses – ‘champions’ we call them. They’re real champions. Even though we weren’t there in person, they were able to spread the word and recruit micro-businesses. Now it’s a network of people helping each other.

- We envisage a world where the economy is owned by the community.

The views expressed in our blog are those of the author and not necessarily lowimpact.org's

What I’ve discovered about the money system and how the world is run, since working with the Open Credit Network

What I’ve discovered about the money system and how the world is run, since working with the Open Credit Network

Community wealth building & mutual credit: a match made in heaven?

Community wealth building & mutual credit: a match made in heaven?

Mutual credit and economic crashes: interview with Laurence Anderson of Tradeswap, Australia

Mutual credit and economic crashes: interview with Laurence Anderson of Tradeswap, Australia

Building the new economy with mutual credit in Costa Rica

Building the new economy with mutual credit in Costa Rica

How ‘chamas’ and mutual credit are changing Africa: Shaila Agha of the Sarafu Network

How ‘chamas’ and mutual credit are changing Africa: Shaila Agha of the Sarafu Network

Mutual credit in Africa: interview with Will Ruddick of Grassroots Economics

Mutual credit in Africa: interview with Will Ruddick of Grassroots Economics

I’ve got a book deal. I’d like to ask for your advice about how to deliver the message.

I’ve got a book deal. I’d like to ask for your advice about how to deliver the message.

Mutual credit clubs: an introduction, with Dil Green

Mutual credit clubs: an introduction, with Dil Green

Two planks – and a bridge – to the new economy

Two planks – and a bridge – to the new economy

Regenerative traditions in Africa: inspiration for the commons everywhere

Regenerative traditions in Africa: inspiration for the commons everywhere

Community

Community

Low-impact money

Low-impact money

Mutual credit

Mutual credit

Commons economy

Commons economy