How do we build a new, non-extractive economy? Dil Green of Lowimpact.org

Today I’m talking with Dil Green, who is a member of the Lowimpact.org co-op. He used to be an architect, and was a founder member of Brixton LETS, and is now on the team of the UK Mutual Credit Network. We’ll be talking about how mutual credit and the viable system model can be used to build a new non-extractive economy.

Dave: Dil, tell us a bit more about how you got to this point?

Dil: I worked as an architect for 30 years, until a couple of years ago. In my study and practice, I came across Christopher Alexander, who had invented a technique called Pattern Languages, initially for addressing architectural design, but which I quickly realised was a brilliant tool for helping us poor humans to map and approach design problems in all sorts of complex systems, including human economics and finance. That helped me get better at understanding systems, dynamics, complex systems interactions. I’ve always been quite ‘alternative’. I was a founding member of a housing co-op 30 years ago (which didn’t go anywhere), and a founder member of another co-op called Brixton Common Land in the late 90s, trying to offset gentrification in Brixton. It still exists and does own a building, although it didn’t stop gentrification. 2 or 3 years ago, I began to be clear that the coming climate emergency, and probable financial emergency, or slow crash, was coming too quickly for architectural work, no matter how wonderful, to be really able to change anything. I was building eco-buildings, but the number of buildings I was going to be able to complete in the coming 10 years weren’t going to amount to ‘a hill of beans’.

So I decided to spend the rest of my productive life, and apply my skills and experience, at a deeper systemic level. After looking around, it seems pretty clear to me that economic and financial systems are at the root of an awful lot of things that are going wrong at the moment. From working with Brixton LETS 20 years ago, and doing Matthew Slater’s Money & Society MOOC, and reading fairly widely, I saw that work was needed there, and that mutual credit was an important plank of that work.

Dave: Yes, I wanted to talk to you about how we build this new economy that’s required, using mutual credit as an exchange mechanism and the viable system model as a governance system. I’ve worked in the environment field for 25 years. We have to stop damaging nature, otherwise the future is going to hold some horrors for humanity. Nature keeps us alive and healthy. We can’t stop damaging nature as long as we have an economy predicated on constantly increasing consumption. We need a new kind of economy – but how are we going to achieve that? The parliamentary route? Can we vote for a different economy? Violent revolution? Divine intervention? Nothing’s looking likely – so how?

I agree that reformism is probably going to be too slow; violence is too risky, and often ends up with unintended consequences of a fairly unpleasant kind, and divine intervention would be lovely, but I’m not going to hold my breath. It’s holocaust day today, and he didn’t step in to stop that, so maybe he’s had enough of us. So I think it’s up to us. Urgent change is really needed, and we can’t hang about, so as I said, I’m looking for the deepest systemic level at which I have the capacity to do something useful.

There’s a woman called Donella Meadows, who was part of the Club of Rome that wrote the original Limits to Growth report in the early 70s, and who carried on doing that sort of work for the rest of her life, thinking about dynamic system change, complex systems and sustainability. She’s written a really good paper that sets out the various different layers of a system in which you can hope to interact – starting with simple things like changing your own lifestyle, and the deepest thing is to change the culture. Looking at my capacities, and where we’re at, it seems to me that the structural dynamics around the creation of money are conditioning at a very deep level, pretty much everything that this industrialised, global civilisation can do.

Very clever people have come up with other ways of structuring and making the rules for a means of exchange that are just as capable of supporting a complex economy, long supply chains, fancy stuff like the computers and technology that we’re using to record this interview, without requiring endless growth to service debt, and therefore without implying capitalism and extractive, unsustainable modes of production.

That seems to me to be worth spending time on. If we can make mutual credit a viable, complementary alternative for many people to spend some or all of their time in – that, just by itself, will change the nature of their economic relation to consumption.

I’m interested in talking about how we federate the non-extractive economy, rather than growing big institutions. Why have attempts at federation failed?

The sort of economies we want to become the norm are ones that are sustainable, and that means living within our means, not continually growing for the sake of growth. So when people set up co-ops or mutual credit networks or other kinds of non-extractive value-creation systems, whether economic or gift economy, by their nature, they don’t have a need to grow rapaciously. When they get big enough, they slow down. That’s exactly what we want to see – we want people to have enough to live decently, but not to feel the need to accumulate more and more and more.

So great – we want to build these systems, but the problem is that capitalism (and not just ‘fat cat’ capitalism – but the whole system of an industrial economy based on debt-based scarce money that we’ve all been living with for hundreds of years) is growing exponentially, and really, the internet and west-coast US venture-capitalist culture has lit the blue touch paper, and the rate of expansion is just spiralling out of control. So we have a real growth problem, and a problem in reining that in with these non-extractive economic modes that we want to replace them with, because they don’t grow fast. So this is where this word federation comes in. What we want is not a growth of scale, but a growth of impact, involvement. We want the non-extractive sector to grow super-fast, and for people to want to actively step out of the extractive, capitalist, rat-race sector and into this non-extractive sector.

So if we can get, within a reasonable amount of time, millions of people, and within decades, billions of people, getting their subsistence from non-extractive, sustainable economies, then that sector has to grow really fast. But it depends on trust, really, and human scale. So it’s got to grow as a network of human-scale organisations. It can’t be a case of 2 billion people on Facebook. That’s not a human-scale organisation. So this idea of federation, of many, many human-scale organisations being able to interact with each other, using modern technology and sophisticated communications and management techniques, to be able to produce things like computers, mobile phones, high-tech medical equipment, so that we can have a decent standard of living. Those are very complex supply chains, industrial processes – all of those things need to be replicated without the huge machinery of capitalism. So federation – wise and effective interaction has to be the way forward.

So how might basing that federation on a mutual credit exchange system and a viable system model governance system work?

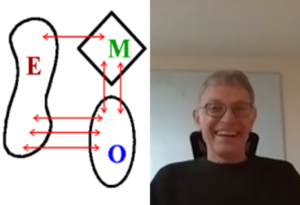

Let’s leave mutual credit to one side for a bit, and talk about this VSM idea – because I know you’ve done an interview with Trevor Hilder, who I know fairly well. VSM stands for viable system model. It’s a fairly nerdy, technical subject, but what it really comes down to is a much more thoughtful and adaptable management model for human institutions, or any system really, than the straightforward management / workers, hierarchical, top-down model that we’ve inherited from the early 19th century, which is very crude. We tend to split people into workers and bosses, and that’s all there is. The VSM is wiser than that in that it says that organisations have to have different modes of operation to be able to persist in their environment and work effectively. There’s production – people doing things; then there’s co-ordination – different sets of people doing things need to be able to work in harmony to produce effectively and without waste. There is of course a command-and-control function there, which communicates to various productive teams what ought to be done next and to make sure that standards and things like that are working.

But as well as those 3 modes that we might understand, it introduces 2 other modes, one of which it calls guardianship, which is about keeping an eye on the reason we’re all engaged in whatever the system is doing in the first place – what is our purpose, why are we doing this? And making sure that short-term goals or environmental buffeting or just inattention, don’t let us go astray, and something we set out thinking was really great might end up existing just for the sake of existing, or existing to make someone rich, or something almost by mistake. So there’s a guardianship function that organisations need. And then there’s another function which is sometimes called future and forward. It’s basically research, sitting back and looking at the wider context, and making sure that surprises, new information from the environment, are incorporated into the action of the organisation in a timely way.

I want to ask specifically how the viable system model works together with mutual credit to bring about this federation of the non-extractive sector.

For me, the VSM model and mutual credit need to also be considered, almost fused together, through this thing that lots of people might have heard of, called the multi-stakeholder co-operative approach, where you look at all the various different players in the system, and you acknowledge that they may have different value propositions – i.e. the reasons they are there are different – and you try to design the functioning of the organisation and the governance of the organisation, so that those different stakeholder groups can all interact together. They all need the organisation to achieve its purpose, so for them to succeed, they need all the other groups to succeed.

Are you talking about the federation itself, that exists as a multi-stakeholder co-op?

This is another key element of the VSM. At every level of the system, you have the same kind of structural thinking. So you have recursion – so within a small work team of 5 people, you might have someone who spends some time remembering the purpose; but when more of those groups come together, you need to have a wider version of all the necessary systems. So if you think of a federation of mutual credit networks, which is what we’re talking about, in order to be able to intertrade between networks, they all have to have access to some accounting system, some trade verification systems, some business directory. Who maintains that? That will be a specialist set of people – stakeholders who will maintain software, deal with handing records to the government and so on, on behalf of all the members. They aren’t the same as an ordinary member who just trades. You get different stakeholders at all the levels of scale. You might have a neighbourhood mutual credit network, a bit like a LETS scheme, where you might trade DIY tools and surplus produce. But then several of those might be joined into a town-sized network with shops and businesses in. Then several towns might be joined in a regional network, and at all levels of this federation you’ve got these different stakeholders. They might be investors – these things will need money to get started. They have very different value propositions from members, and so we need to align all these people very carefully.

There’ll be some things we can’t get from the non-extractive sector yet – like laptops or cars. What do we do then – just suck it up and do the best we can until we can get them from the non-extractive sector?

There isn’t really anything else we can do. At the moment, in the UK, pretty much all the electrical power is generated by huge, international businesses. We’re not going to change that overnight. So for the first couple of phases of building this new economy, we’ll have a mixed economy, where we’re holding our noses and doing business with organisations that we think are probably, on balance, destructive. We have to live. The key for me will be making it as easy as possible at every stage, for the next target group of conventional businesses to be able to transition to mutual credit – either fully or partially, as they go along. I’ve been thinking about this with banks, which are closing branches all over the country. One reason they’re doing that is that they’d really love to have no cash. They’d love to have a cashless society, because it’s very cheap for them to run that – they could sack a huge proportion of their staff, and just run everything with computers and a few hundred people at head office, with everyone using smart cards to pay for everything. But actually, that’s a two-edged sword for them, because mutual credit works purely on information. It doesn’t have physical tokens, like cash. So actually, once the banks implement those systems, then at a certain level of scale, we can invite them to become servicers of mutual credit. They won’t earn interest, so they’ll have to make their money doing something else. But here comes mutual credit – it’s a growing thing. Those sorts of things are fun to think about now, not very seriously, but in the future, that will be the way to think.

I guess a non-extractive economy will involve co-ops of various descriptions, sole traders and public sector workers? Anything else?

Co-ops are the obvious place to start. There are a number of great things about working with co-ops, beyond the obvious reasons. Co-ops have immediate access to members, because all of the workers in a co-op are members of the co-op. We’re planning to start this UK Mutual Credit Network as a business-to-business network, but to expand throughout the economy, it needs to be able to serve individuals, and the individuals within a co-op, that’s in the mutual credit network, will be a great place to start. At the other end of the spectrum, the co-op movement already has access to government – it can go and talk to government and tell it what we need. So the co-op sector’s great.

The public sector is another brilliant target, that we’d be looking at a lot sooner than at energy generation companies, because most of the work that local authorities do is labour power. They employ local people to deliver local services. That’s tailor-made for mutual credit, and in an era of austerity – even if the cash floodgates are opened – it’s still going to take 15 years for local authorities to build their services back up to where they were in 2010. So mutual credit networks can massively leverage the power of local authorities to do great work.

So sole traders – they’re basically individuals on steroids, really. Probably the main issues there will be annoying ones like their regulatory status, and whether this counts as consumer credit. So for sure, all of those sectors should be folded in within a reasonable timescale. Once you get local authorities, you can next look to hospitals etc, then suddenly you’ve turned a huge corner, because those organisations employ tens, hundreds of thousands of people. Once those employers realise what they can do with mutual credit – how it completely unlocks the constraints of scarce money in delivering the services that they strongly believe in as a social good, that will be enormous.

And how do we keep the individual units of this new economy small, and federate them, rather than allow them to grow huge? I’m thinking of the Co-op Bank in particular, which grew huge, stumbled, and got swallowed whole by a hedge fund, and suddenly there’s no co-op bank in the country. If it had been a federation of small, local co-operative banks, then if part of that federation fell over or got bought out, then we’d still have the rest of the federation. How do we keep the units small?

Probably, constant vigilance. On the other hand, it seems clear to me that mutual credit, at least to start with, is going to be less economically useful than the pound in your pocket, which can be spent on anything that’s for sale in this country. In a mutual credit network that’s just starting out, with a few thousand members, you’ll only be able to be spend on the things that those few thousand members provide, and that’s going to be limited. So as a purely economic means of exchange, it’s not going to be as good as pounds for some time to come. So what makes it better? We have to look to things that are not purely economic, and those are: trust, community, solidarity – and it turns out those things are economically useful as well. You’ll give more credit into a network where you know that the people in it are people you’ve met, and you understand their ethos, than you would to an anonymous, corporate exchange network.

So I think there’ll be a natural tendency for these networks not to grow too big. As I’ve said before, the nature of non-extractive economics is that people tend to grow until they’re happy, and then just stop – whereas extractive businesses try to grow and grow and grow.

They have to keep increasing returns to their shareholders, don’t they?

Yeah. And also, because they’re in a competitive environment, even if you run, say, a cafe, and you think you’ll just run it until you retire, because you make a decent living and you like your customers – but suddenly on one side you get a Cafe Nero and on the other a Starbucks, and your business goes. So people feel that they have to grow, even if they don’t want to, in the capitalist sector. So we need to leverage this social side of the mutual credit networks, and that will tend to limit the scale of the individual networks. People will like to be in networks where they know they can trust people, and that will give them a value that adds to the pure economic value of the currency units that you get.

It adds to their quality of life?

Yeah. I was active in Brixton LETS scheme for four years or so – but it stopped being a viable network for me about 20 years ago, and I stopped being an active member. But the acquaintances that I made through the trading that I did over those years have lasted me 20 years, and I’m knitted into the fabric of Brixton. I have this great network of acquaintances, and when I see them, I don’t have to say ‘oh my gosh, we haven’t seen each other for so long – we must meet up more often’ – I can just say ‘hi, haven’t seen you for a few years – how are you doing?’, and you have a chat, and you’re just happy that they’re there. It’s a big thing, in modern society.

What will be the biggest barriers to this kind of approach, do you think, and how might we overcome them, or get round them?

Lots of barriers. The biggest might be the stuff inside people’s heads. We’ve had hundreds of years in the West of scarcity-based money, debt-based money, monopoly-controlled money, commodity ideas about money. Those things have worked their way into the culture. They’re part of the way we grow up, thinking about how money has always worked. When you say to people that it doesn’t have to work like that, they sometimes get a bit leery. If you say: ‘I know more about money than you do – if you join in with this new scheme, it will be very good for you’, people will think ‘hmm, here’s someone talking about something I don’t really understand, and they want me to invest time or effort into it – I think I might get ripped off here’. That would be a standard response that people might have. We’re going to have to develop a lot of soft culture around what mutual credit is.

Maybe we need more accessible information – videos, talks, books, blog articles…

And games, cartoons, stories, comics, films – it’s probably going to take hundreds of years for some of the deeply-ingrained feelings about money that this culture has, to work themselves through.

Also, the extractive sector are going to want to keep extracting, and they have a lot of power. What’s to stop them buying up parts of the federation, or leaning on governments to legislate against us?

First, we have to craft our legal constitutions, checks and balances and governance agreements really carefully. That’s crucial – so that what happened to the building societies can’t happen to us. We have to put these poison pills into our constitutions, that make it not worth the bother for financialising institutions to come and try to rip the value out of the networks. As to legislation, stacking the decks against us, that’s bound to happen. If you look at the history of mutual, solidarity finance institutions that the working classes have built, like building societies, mutual assurance societies etc. – the kinds of things that the disadvantaged tend to group together and build – any of those that become successful tend to attract lots of legislation, which are framed as: ‘there have been some failures in this sector, and some people have lost their savings, so you can run a mutual bank, but you have to have £20 million as collateral before you can open it’. That sort of thing is bound to happen. So what we have to do I think, is to frame the legal structures of our organisations as closely as possible to existing organisations, so that if they try to legislate us out of existence, they’ll also be legislating conventional businesses out of existence.

Where do the resources come from to make this all happen?

We have to sort of build this out of thin air. We’re saying that we’ll build a sector that won’t produce massive profits. It’s a non-extractive sector. That means it will be difficult to get the kind of investment you might think of for building a different kind of business to come in. However, there are some very smart people around. A chap called Chris Cook, who’s on our advisory panel, has come up with this particular approach, which allows investors to get a fixed rate of return, and only on the basis that the project succeeds. So there will be a vehicle for patient investors, who share the same analysis of impending slow crashes in the environment and the financial system, and who want to build a resilience against that, to make hard cash investments that will repay them decently in hard cash terms, as the mutual credit system expands. I think we can design legal and financial systems that will make those investments attractive enough, and safe, in terms of not giving away control or ownership to people who are only putting in cash.

Do you honestly believe that there’s widespread support for a movement like this?

No, I don’t think you could call it widespread. I think the door is there to be pushed open in progressive financial circles – progressive economists, people like Positive Money, Good Money, Rethinking Economics, New Economics Foundation, Kate Raworth’s Doughnut Economics. There’s a lot of new oxygen in economics for non-orthodox apporaches. There’s an amazing woman called Stephanie Kelton in the US who’s pushing modern monetary theory ideas, which are half-way towards mutual credit to be honest, all the way to quite right-wing business people, who are giving mutual credit quite a good reception. So I don’t think the general public, or chief financial officers in business circles, have any real clue what mutual credit is, but I think the chances of us getting good support and constructive engagement with the progressive finance and economics communities are pretty high. And that I think will lead to some investment, and probably to some regulatory simplification. If we get support from people talking to government, that should help.

To be honest, I don’t think widespread support is going to come until people’s friend tell them that their business is trying this new ‘funny money’ stuff, and you know what – it’s working. It’s going to be not so much about support as about people voting with their feet when they hear their friends saying that they’ve joined a scheme, and their turnover is up and their debt payments down.

I guess it will take off when it’s established, and easy to join.

It’s chicken-and-egg – how do you get there from here? We’re going to have to start with enthusiasts, with people who really want it to work, with people who share our analysis, and we’re going to have to plough through a couple or three years of fine-tuning things, pump-priming, building networks, refining the software, the accounting, to make it as easy as possible to use. That’s why I think we need to be thinking about raising finance to get us through those periods. We can’t work in a ‘pull ourselves up by our bootstraps, even if it takes 20 years’ modality, because capitalism’s growing too far and too fast, and the climate’s collapsing too far and too fast.

I suppose if it works, it will be quite exciting to have been an early adopter.

Sure – being an early adotper is always an interesting thing. There are ups and downs, but designs and methods we’re thinking of, allowing businesses to participate in a mutual credit network, are carefully structured to avoid anyone getting seriously burnt.

One final question – do you think we have enough time?

It doesn’t matter – we have to do it anyway. It’s the Transition Town argument – will that kind of thinking save our civilisation? We don’t know, but if we don’t try, it definitely won’t work. And if we do try and it fails, who do you want to have been working with – the people who have been building resilience, or the people who’ve been working to destroy things? I want to be with you guys, whatever happens.

OK Dil, thanks very much for the chat.

Thank you.

NB: Dil would like to encourage readers interested in more detail as to how a federation of mutual credit networks might build a wide and deep economy to read Matthew Slater and Tim Jenkin’s 2016 whitepaper, “The Credit Commons – A Money for the Solidarity Economy.

About the author

About the author

A Director at Lowimpact.org and NonCorporate.org, Dil Green was an architect and builder for 30 years, working on projects from an extension to London’s Science Museum to an award-wining eco-surgery. He now works away at systemic leverage points around Governance, Wisdom: Pattern Language, and Economy: the Open Credit Network, . He lives in Brixton and blogs at digital-anthropology.

Highlights

- The sort of economies we want to become the norm are ones that are sustainable, and that means living within our means, not continually growing for the sake of growth.

- For me, the VSM model and mutual credit need to also be almost fused together, through the multi-stakeholder co-operative approach.

- We have to look to things that are not purely economic, and those are: trust, community, solidarity – and it turns out those things are economically useful as well.

The views expressed in our blog are those of the author and not necessarily lowimpact.org's

16 Comments

-

1John Harrison February 3rd, 2019

Couple of points from the section “They have to keep increasing returns to their shareholders, don’t they? ”

First the system is weighted in favour of big business – companies like Cafe Nero and Starbucks play the tax system and economies of scale, shifting funding around the world. So Joe Bloggs Coffee Shop is disadvantaged to start with. To level the field requires governments with the strength to fight multi-national corporates.

Secondly – there’s a business axiom that you’re either growing or shrinking. In other words you have to grow (by improving) to survive. Also it’s human nature – especially for the self starters who tend to own business – to want to achieve more. They want to sell more coffee, open a second shop, open a chain of shops, conquer the world…

Replacing the current failing and insane system of infinite growth does need to take into account that there are those who are content to plod along and those who want to do more. Incidentally, there’s nothing wrong with plodding along – it really does take all sorts.

-

2Dave Darby February 3rd, 2019

John – sure, we could wait until an electable party comes along with the will to challenge the corporate sector. But this article is about building an alternative ourselves, without waiting for government. If it happens, great, but personally, I think it will be a very long wait.

And you have to be very careful I think, when talking about ‘human nature’ – very difficult to work out what’s nature and what’s nurture. There are humans that are satisfied with one business that gives them a living, therefore the desire to open chains can’t be human nature. And the axiom you talk about only applies to capitalism. We need an alternative, with businesses that don’t need to grow to survive.

-

3John Harrison February 4th, 2019

As you’ve basically said before, Dave, the corporates have bought government so it’s a forlorn hope I have that the field will be levelled.

Actually, whether nature or nurture, I think you prove my statement. ? The innovators, those at the front, are the sort of people who want to build and create something more. You could be satisfied with setting up something at a very local level but no, you want to replace the whole damn system. And I really hope it happens.

-

4Malcolm purvis February 4th, 2019

Very interesting article, thank you Dave and Dil. There is a lot to take in here with VSM, and the concept of mutual credit.

I would like to see a vision for this movement which is not yet clear for me. That is probably because at the beginning and perhaps for some time, it will be very much linked to our dysfunctional present money system and have ‘investors with a fixed rate of return’ ie shareholders. There will need to be very careful monitoring of this so that these shareholders do not become the customers of this system as we have with the corporations at the moment. We could easily have pension funds etc wanting to invest in this and they would have no other interest other than profit, would we say no sorry you cant invest in this, we wont take your money?

So, what is the vision please? Many believe that if you have a strong vision that the law of attraction will manifest it for you and this would be a great leverage for mutual credit. Many people will know ‘The Secret’ book by Rhonda Byrne, also a video/film. The book has sold more than 30 million copies, which tends to indicate that it is pretty good, all about the law of attraction and how we can make things happen/materialise.

With Johns point that there is a business axiom that says ‘you are either growing or shrinking’ highlights the fact that we really do need to re-think our belief systems. Our belief systems shape our world and these have to change as they are not working and are also untrue, we have to uncouple from the belief that money is one of the most important things in our life and will make us happy! As Joanna Macey said ‘ we have had 8,000 years of an agricultural revolution and 200 years of an industrial revolution and we are now on the cusp of ‘The Great Turning’. These things can happen very quickly as evolution has shown us that it happens not in a gradual slope but as step changes. Many people believe that we are at a similar point we were at when we crawled out of the sea to live on land!

So, mutual credit might be our saviour if we can have a real solid vision and manifest it. Real change is coming, let’s all hope so.

-

5Dave Darby February 4th, 2019

Hi John – yes, I definitely do have ambitions around the ‘growth’ of an idea. I guess the distinction is around the word ‘more’. More intangibles – ideas, artistic ability, spirituality, love, philosophical thought – all these kinds of things can grow indefinitely; but the economy, in terms of GDP, definitely can’t. I’d like to see that awareness grow too, so that I no longer have to listen to a discussion on Radio 4 about how we’re destroying the ecosphere, followed immediately by a discussion on how we’re going to increase economic growth.

-

6Dave Darby February 4th, 2019

Malcolm – ‘I would like to see a vision for this movement which is not yet clear for me.’

You’re not alone! We’re working on it. There’’s a meeting coming up of people in the non-extractive economy, to work out if and how we can use this combination of mutual credit and VSM to get it to grow. I’ll report here.

(you can’t extract profit from a mutual credit system though).

(have to tell you though – I really hate books / movies / whatever like ‘the Secret’. There’s one every 10 or 20 years – if the Jews had just ‘thought positively’ the holocaust wouldn’t have happened, and if Syrians could just visualise peace, starving children visualise food etc….. Sales don’t indicate quality – the most popular newspaper in the UK is the Sun, and so on. I think Dave Chapelle nails it).

https://www.youtube.com/watch?time_continue=142&v=WbS9jZOlQjc

-

7John Harrison February 4th, 2019

What really confuses me is that they say we’ve had economic growth every year (near enough) yet people don’t seem better off here in Britain. Or maybe that’s just the gap between rich and poor growing. Whatever, this is not the future I wanted or expected.

-

8Malcolm purvis February 6th, 2019

Dave, thanks for your reply. I’m a little confused though, Dil says that ‘investors’ would be needed for a mutual credit system. The definition of investment is that there would be a profit so I’m not sure how this works? It would surely be very difficult to get many people to ‘invest’ with no return especially as at first you would be running alongside the money system, but you say there would be no profit?

I respect your views regarding the law of attraction and your right to express them but I don’t agreee with them. ‘The Secret’ is just an example of a book written about the law of attraction of which there have been many over more than a hundred years. The law of attraction has been used for many decades by Olympic athletes, many sports people and businesses. Most people would see that if you have a clear vision and stick to it that you have a good chance of success. ‘The Secret’ gives a lot of very accessible ways that this can be achieved and that is probably why it has been so successful, I’m not saying it is perfect by the way. Obviously if you don’t believe in it and have a Cartesian world view it wont work but I can assure you that I have personal experience where it has been a phenomenal success on many levels. Certainly not something that should be dismissed by cheap jokes in my view.

Keep up the good work though and good luck with the mutual credit project.

-

9Dave Darby February 6th, 2019

Malcolm – thanks for keeping the two subjects separate! Not agreeing is fine. Blogs would be quite boring if there were no disagreements.

There are different kinds of investors. For example, I’m an investor in the Ecological Land Co-op – a multistakeholder co-op, along the same lines as the entity we want to set up. I have community shares that are capped at 3% return (which isn’t bad), but I can’t sell them, and I don’t get control of the ELC by getting 51% of the shares. It’s one person, one vote, not one pound, one vote. ‘Profit’ tends to mean unlimited amounts that can be extracted from businesses, and is usually the aim of the business in the first place.

The Secret, and other books like it, make me quite angry. Dave Chappelle’s joke wasn’t cheap – it cut right to the heart of it. Telling people that their problems are due to a lack of positive thinking or visualisation is deeply insulting to people living in extreme poverty around the world – blaming them rather than the damaging system that they live under. Apart from being anti-scientific, it’s also racist – people in poor countries (usually darker-skinned people) just aren’t thinking positively enough to escape poverty, and in some cases starvation. It’s their fault. A million times no. Yes, there have been plenty of preposterous books like this one – as I said, one comes out every 10 years or so. It distracts people from the fact that our economic and political systems are the root of the problem, and in fact, what most people look to these quack philosophies for is to make more money, and actually make the systems worse. This nails it – https://markmanson.net/the-secret. (and it doesn’t mean that you’re a Cartesian – I’m not – if you recognise bullshit when you see it).

-

10Malcolm Purvis February 6th, 2019

Dave, good to get your comments. I think that there is a lot of misunderstanding here by Marksmanson and yourself. Nobody is saying for one minute that all peoples problems are a result of their negative thinking or that all people can escape poverty in poor countries purely by thinking positively. I agree with you ‘a million times no’ that it is not their fault. However, just because people achieve things by visualisation ( I have many times and so have millions of others) that they are ‘delusionally positive’ as Marksmanson says is ridiculous. One of the great things about the law of attraction is that you can have great fun with it and just see if it works, its not a dogma, but if people think they can have a positive life by thinking negatively then I would say they are delusional. And as for being realistic as Marksmanson states, I would say that is the most commonly trodden path to mediocrity.

Marksmanson says that “thinking about things you don’t want leads to more negative thinking”. This is one of the basic precepts of the law of attraction and is very true, what you think about you bring about. This seems to indicate that Marksmanson has not read about the law of attraction properly or maybe not understood it and what it is saying.

Anyway, good banter Dave and we can agree to disagree. But, if you want the mutual credit to be a success, and I certainly do, I would be amazed if you can achieve that without a very clear vision of what you want to achieve and a positive thought that you can achieve it. If you do this and are successful you may just have proved that the law of attraction works………

-

11Dave Darby February 7th, 2019

Thanks Malcolm. I guess I’d just call that ‘trying to do something’. I just visualised a cup of tea, and then successfully attempted to make one. But if I’d visualised something less realistic, like beating Usain Bolt in a sprint, no amount of positive thinking is going to achieve that.

But yes, we’re definitely, definitely going to try to implement a UK mutual credit network, and if you could help us with lots of visualisation and positive thinking, that would be much appreciated! ?

-

12Malcolm Purvis February 8th, 2019

Dave, I will certainly help all I can. I don’t want to prolong this thread beyond its useful life but I would like to make a couple of important points please.

The reason that people who are starving and poor (and many others) cannot use the law of attraction is because of Maslows Hierarchy. This has been completely ignored by Markmanson et al in order thereby to make a completely skewed (cheap) argument and would not therefore ‘nail it’ in any way shape or form for most people.

The subconscious mind is approx 95% and the conscious mind 5%. So the vast majority of our thinking, actions, beliefs etc etc are done subconsciously. The law of attraction can be utilised to programme the subconscious mind for us by giving it a belief system in whatever we want to achieve. It does need a real desire and drive especially if it is a big desire/project like running a sub 10sec 100m or setting up a credit commons, it does also need some integrity/sincerity. So, asking Usain bolt to set up a credit commons would be like you being asked to run a sub 10sec 100m. This is not to say that either of these things cannot be done, I’m sure that the merchant bankers et-al (not me I hasten to add) might say that you maybe have more chance of running a sub 10sec 100m than setting up a credit commons for the whole of the UK. Usain bolt might also have a real desire for a credit commons? Stanley Mathews played football at the very top flight when he was 50 years old, and afterwards said he retired too early!

We certainly haven’t yet reached the limit of what the mind and body is capable of, given the desire etc.

What and how we tell our subconscious is also important and Cassius Clay was a prime example when he said ‘I am the greatest’. In most peoples minds he became the greatest. He never said ‘I will try to be the greatest’! It all works if you feel like you already have it and believe it/feel it (belief system). Of course it also works the other way, so if you have a belief system that says all this is rubbish that is also true as Henry Ford famously said.

So, ‘We are going to implement a UK mutual credit network which will develop into a worldwide scheme in 5 years time involving 1 billion people’ !! Does that not fire you up and give you goose bumps?

-

13Dave Darby February 8th, 2019

Malcolm – It certainly does.

So, using the principle of ‘Pascal’s wager’…….. We are going to implement a UK mutual credit network which will develop into a worldwide scheme in 5 years time involving 1 billion people.

Feels good.

…….

…………. however

………. (and we do have to leave this for another thread, as it’s way off topic)

I’ll say the same thing about the ‘law of attraction’ as I say about the ‘succussion’ part of homeopathy. As I don’t have the ability to carry out research myself, and as Lowimpact exists because of what scientists are saying is happening to ecology, my beliefs or lack thereof will be completely down to what the scientific community has to say about it. And if you look on wikipedia, it says that there is no scientific basis for it at all – that it’s pseudoscience based on anecdotal evidence. You could go in to try to change the wikipedia entry, but I don’t think you’ll be successful. Sure, there are breakthroughs from time to time that turn science on its head – such as Einstein’s – but they are demonstrable, and the scientific establishment changes its perspective immediately (which is exactly what it’s supposed to do, of course). People generally don’t become scientists for financial reasons – they do it because of curiosity and a love of knowledge. I don’t believe that they are corruptible in the same way that, say, politicians are. So at Lowimpact.org, it’s a policy that we rely on peer-reviewed science for our claims about the nature of the universe, whilst of course looking for corruption where we think it might exist (2% of climate scientists, for example?). We don’t have the time, the ability or the inclination to do anything else, I’m afraid.

I think this could be an interesting blog post – why we have to listen to scientists about climate change and ecological damage – because the peer-review process, when done properly, is the best reality check we have.

-

14Malcolm Purvis February 8th, 2019

Dave, very pleased that you like that and I also like your Pascal’s wager analogy. I of course believe that you could quite easily ‘prove’ in your own mind whether the law of attraction works or not by trying it out a number of times, with a real belief, and seeing how often it works, or not. I personally have found it to work extremely well, it is not a scientific thing obviously so it is not like a computer programme that works every single time (and we all know that even computers don’t always do that) but try it for fun and you may be astonished.

You may laugh but I always dream/visualise a perfect parking place when we go to a busy car park or street etc (I call it my parking angel….). It works an amazing amount of times, I would guess 8 or 9 out of 10 and my wife always laughs like a drain every time it happens. This is a common law of attraction experiment and is just great fun. You can also do it with a cup of tea/coffee and visualise it very clearly (not by making it yourself) and wait for it to ‘pop up’ sometime in the not too distant future (that day), again great fun.

Best of luck and I will look forward to your future blog posts.

-

15John Harrison February 8th, 2019

Glad to hear your visualisations work for you Malcolm. Visualisation is, of course, an established method in magic, you may like to read Initiation into Hermetics by Franz Bardon or somewhat lighter, The Training and Work of an Initiate by Dion Fortune. I don’t recommend raising demons to secure parking places though, even in London.

Dave – Being serious, I do worry about the objectivity of some scientists based on the responses I had for daring to question the safety of Glyphosate. Which was ironic as I was also being attacked as a tool of Monsanto by others for the same article. Obviously climate change is a hoax and the scientists and Met Office are in the pocket of those rapacious green tree-hugging hippies. ?

Fact is, most of us are unable to properly evaluate and, as you say, peer reviewed science is the best reality check we have.

-

16barefoot doc April 11th, 2019

Dil, d’you have links of your own for how to do pattern language? Is it still a feature of your work or have you left it behind since leaving architectural practice? Seems to me it’s a hugely significant way of handling practice-based knowledges of ‘building’ in the broadest sense, accumulated thro traditions and movements, and played out in fresh ways in fresh situations. But exploited quite rarely.

I’m at work on a pattern language for commoning. Would be glad to have an exchange on this.

How the viable system model (VSM) can help build a new economy: Trevor Hilder of Web of Wealth

How the viable system model (VSM) can help build a new economy: Trevor Hilder of Web of Wealth

Free online course: Toward Co-operative Common Wealth MOOC

Free online course: Toward Co-operative Common Wealth MOOC

Developing local entrepreneurs and keeping out giant corporations: Jay Tompt of the REconomy Project

Developing local entrepreneurs and keeping out giant corporations: Jay Tompt of the REconomy Project

Moving towards post-capitalism, or: why I’m working on mutual credit

Moving towards post-capitalism, or: why I’m working on mutual credit

Does anybody fancy a free, one-day course on the viable system model (VSM)?

Does anybody fancy a free, one-day course on the viable system model (VSM)?

UK Mutual Credit Network: register your interest

UK Mutual Credit Network: register your interest

Why the future of money is mutual credit (and not Bitcoin): Interview with Thomas H Greco Jr.

Why the future of money is mutual credit (and not Bitcoin): Interview with Thomas H Greco Jr.

What are ‘the commons’ in the 21st century? Interview with Pat Conaty

What are ‘the commons’ in the 21st century? Interview with Pat Conaty

The alternative to the current money system: Tim Jenkin, Matthew Slater & Dil Green

The alternative to the current money system: Tim Jenkin, Matthew Slater & Dil Green

Mutual Credit Services – keeping communities alive after COVID: explaining the Credit Commons Protocol

Mutual Credit Services – keeping communities alive after COVID: explaining the Credit Commons Protocol

Mutual Credit Services – keeping communities alive after COVID: Trade Credit Clubs and credit clearing

Mutual Credit Services – keeping communities alive after COVID: Trade Credit Clubs and credit clearing

Co-operatives

Co-operatives

Commoning

Commoning

Community

Community

Fair Trade

Fair Trade

Low-impact money

Low-impact money

Low-impact shopping

Low-impact shopping

Mutual credit

Mutual credit

Commons economy

Commons economy