Tom Woodroof of Lowimpact and Mutual Credit Services talks with Tomaž Fleischman of Informal Systems about credit clearing. We believe that credit clearing is one of the four crucial tools in building a new commons economy. Below is video and a transcript of their conversation.

Here’s some background, to help you understand more about the concepts discussed.

There has been a national-scale credit clearing scheme in Slovenia since 1991. Here’s an article about that. Tomaž has been involved with this scheme for many years, and is now working on the technical infrastructure to set up similar schemes elsewhere – nationally and locally.

Liquidity-saving = reducing the need for cash / fiat money.

Credit clearing means that payments between businesses can be ‘cleared’ if loops can be found, in the same way that if I owe you £10 and you owe me £10, then we can just clear it and neither of us has to find £10.

Introduction to the topic of credit clearing.

Multilateral obligation setoff (MOS) is a type of credit clearing explained in the introduction above.

The four crucial tools involved in building the new commons economy.

Introduction to mutual credit (credit clearing can be a ‘gateway drug’ to mutual credit, if you like).

Interview with a specialist on the history of credit clearing.

Local Loop Lancaster & Morecambe – credit clearing project that MCS and Informal Systems are working with.

TW: How did you get into this work?

TF: Coincidence, more or less. I was working with colleagues who invented the system that’s been used nationally in Slovenia since 1991. We discussed it a lot – what were the local, national and macro implications of the idea, and why was it only working in Slovenia? Why hadn’t it spread to other countries? These initial investigations turned into a career! The concepts were being thought about most in the world of complementary currencies, and so I searched for successful examples. I discovered the work of Guiseppe Littera and Paolo Dini at Sardex, in Sardinia.

We wrote an paper on credit clearing and mutual credit that became much more successful than we anticipated, and it kick-started my career in alternative finance.

Yes, that article was a revelation to us at Mutual Credit Services. Could you tell me a bit about the history of credit clearing in Slovenia? Was there anything special about Slovenia that enabled it to happen there?

In 1991 Slovenia broke away from former-Yugoslavia. The system was used in a more basic form in Yugoslavia previously. The credit clearing system was available not just to banks (as in the West), but to everyone. Slovenians were used to liquidity-saving mechanisms. Early iterations were not very efficient – as computers were not as advanced as they are now. But mathematically, it was very efficient – as in, it’s impossible to save more liquidity using any other method. This made the Slovenian system work very well for people. But it was also the timing. We were a new nation, not recognised by the global community. We didn’t have a national currency. We used coupons that were printed on left-over paper from coupons that were printed for the winter olympics in Sarajevo. These coupons had no names, dates or signature of a central bank governor. We used these coupons for one year. It was a tough time. In these circumstances, alternative ways to settle obligations / debts were more than welcome.

In the first year of operation, this system saved approximately 7.5% of the country’s GDP. I’ve never heard of an alternative financial system that’s had such a huge impact on the national economy.

We knew from people like Hans-Florian Hoyer that credit clearing has a long history, but when we came across your work, it was the first time we’d seen anything like this, at this scale in the modern, real economy. The idea that there was a country in which these ideas played such a huge role was mind-blowing. What were the steps that allowed this to be used in the real economy before 1991?

I’m too young to have personal experience, so I can just tell you what was explained to me by colleagues. Financial discipline in Yugoslavia was not good, and MOS was useful in releasing some pressure between different members of the federation, and allowing transactions that otherwise would not have happened. Debts were recorded on paper, and copies were sent to the Central Accounting Agency. Yes, credit clearing is an old idea, but states hadn’t been involved like this before.

The reason we were excited about this is that it’s simple and lower risk than mutual credit, and so you can bring large numbers of businesses into these collaborative relationships relatively quickly, without their having to take on too much risk. Can you tell us more about its usage in Slovenia since 1991?

Usage since 1991 is steadily declining. The financial value to individual players is relatively low – somewhere between 7-12%. But this is the average. Some players receive huge financial benefits, but most have slightly less than average. Large, centralised hub businesses benefit more than individual players on the edges. A huge benefit for Slovenia is the reduction of risk in the system as a whole. This creates a more stable financial environment, with more opportunities for businesses. It’s easier for banks to provide finance because of the lowering of risk. Reduction of risk is the most important economic impact for the country, I think.

This is a state initiative, but participation is voluntary. Not everyone participates, but many do because of the benefits of improved relationships between participants. If you ask participants about the benefits, you hear things like improved cashflow, payments received earlier. So this improves relationships with both customers and suppliers, and suppliers can often provide better terms because of this and participants are happier to do little favours for each other.

So for businesses in Slovenia, I think the biggest benefit is the improved relationships with other businesses – both customers and suppliers. These benefits increase over time.

Are the benefits more obvious to the government than to small businesses? Does the government find it difficult to get businesses involved?

Financial institutions are not so interested, because they see it as something that can reduce their profits / eat into their business. So the finance industry isn’t pushing for it. But nation-states and central banks are interested, because they see it as a risk-reduction measure and a way to intervene in the market in times of crisis. It adds a new instrument to possible interventions that have typically included interest rate manipulation and quantitative easing – tools that are limited and imprecise. MOS / credit clearing can be precise, but difficult to implement. Problems of implementation are the biggest barrier. For most small businesses, the strength of globalisation, with its long supply chains means that many of their trading partners are not local. This makes implementation of local MOS schemes difficult.

But there are remedies. I think the biggest one could be the involvement of locally-important projects for local resilience. Being part of a global system with long supply chains carries a lot of risks. In response, there are trends towards building local resilience in terms of energy and food security, and local jobs. For the global finance industry, these projects are simply not profitable, so it’s hard to get commercial finance from the banks. They’re often reliant on government subsidies – which is a very centralised, administratively complicated process.

Combining local business networks with local initiatives that help create local value circulation, empowering those local business networks with tools like MOS. This is the way to go, I think.

That’s certainly the direction Mutual Credit Services is working towards. We have the Local Loop Lancaster & Morecambe project in Lancashire. We can talk about that more – first I’d like to talk about other collaborative finance tools, as well as MOS. But before we do that, have there been any other attempts to implement the system in Slovenia at a national level?

Slovenia has been the most successful, but it’s not the only one. There is something similar (but with different algorithms and techniques) in Romania, and there are things happening in Bosnia-Herzegovina. I don’t know of any other national-scale projects. But there are a lot of local projects, for example in Italy, Spain and the Netherlands. Portugal introduced legislation in 2019. Their ideas was not to run this as a govt. agency, but to seek a public-private partnership. The legislation helps in setting up these schemes. But as yet, they haven’t been able to find partners to run this at the national scale.

So implementation is key. What are the requirements for setting up a successful local scheme?

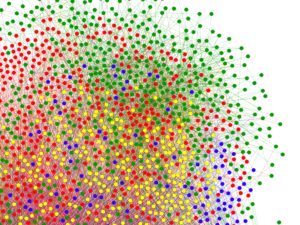

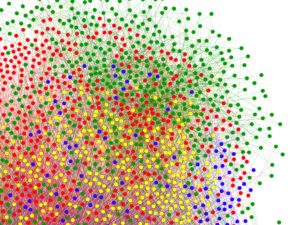

The crucial element is the existence of trading loops between local businesses. Often, local business networks are chaotic, and it’s difficult to find loops. Our experience is that as a network grows, at some point, there will be what mathematicians call a ‘phase transition’ – suddenly, loops appear everywhere. It’s like a switch – there are no loops, then suddenly, they’re everywhere. Reaching this point is the challenge for grassroots projects. Interestingly, it’s not about the number of participants, it’s about the density of the network. What you’re looking for is on average, 2-3 (and ideally, more than 3) obligations between network members. If this is the case, you’ll hit the phase transition point relatively soon. So you don’t need thousands of business. If there are maybe 50-100 businesses with more than 3 obligations between members, you’ll reach the phase transition and find loops.

Can you say more about the dynamics of these networks, and what has surprised you / continues to surprise you?

These networks tend to be chaotic. Firms are connected to each other randomly. But there are rules – the most important being the ‘preferential attachment’ rule. It’s a simple rule that states that a new participant in the network is more likely to attach to big players in the network than small ones. The result is that you get a highly-connected network that is clustered, with distinct ‘hubs’ represented by big players. These hubs are connected to each other, so that the whole network becomes connected, and that there are very few steps between any two participants (maybe 4-5 steps), because a lot of traffic goes through the hubs.

A bit like the ‘six degrees of separation’ concept?

Yes. This actually works because of the preferential attachment rule. Steps between people / participants can be surprisingly short. With the six degrees concept, the average number of steps between people is the logarithm of the number of participants. So a network of millions of people still has a very small number of steps between members.

So with a business network, it can keep growing, but members are still closely connected. But the preferential attachment rule can mean that the hubs get bigger – the rich get richer. There can be inequality, in that some members are strongly connected and others are at the fringes. Have you found this, and what’s the solution?

The algorithms used don’t support the idea of governance. So how to choose an outcome that benefits the most network participants, but still manages to clear the maximum amount overall? We have to make sure that no-one has any influence on the outcome, but for small communities, concentration of benefits in large, hub businesses isn’t idea. So we’re working on ways to include some sort of governance possibilities, where communities could set their priorities. This has to be done very transparently, otherwise it could become a tool to manipulate the economy.

What would be the options then, for a community running this for themselves? What choices could they make?

First they have to decide what’s more important for the community. For example, if food safety is most important, it could be set up to increase benefits to members actively involved with food safety.

This is exciting for us. We want to set up schemes as clubs, being run by and for their members, on a commons governance basis. Having people like you working on the technical requirements to underpin that decision-making is invaluable. We’re trialling this idea in Lancashire, but our model is to franchise the platforms we create. We like the idea of large numbers of relatively small, self-governing groups, making decisions about what they prioritise in their communities. There’s an interesting trade-off between being small enough for commons governance, and big enough to have a viable network.

Size isn’t everything. For small communities there are huge opportunities to be creative in how they use credit clearing. It can provide liquidity to the community (without doing anything illegal!), but you have to find local trading loops. A local community initiative can form, with the intention of purchasing what they need locally, within the credit clearing / MOS group. The funding and goodwill to support this group is multiplied within the network. The community can help form local trading loops within networks, that help to build infrastructure and initiatives that provide things that the community needs. The networks are very social in character, and can be launched by a few ‘activists’ in ways that bring benefits to the whole community.

This implies that people could make a living by setting up and maintaining these kinds of networks, building the kinds of things that their community needs? It’s not being run remotely, in a technocratic manner by experts / the government etc. It allows local people to decide the priorities for their locality.

I agree. And a large enough network can be self-sufficient, funded by tiny transaction / service fees. It also means that any money provided by the local authority will go further – which will make them very happy.

MOS / credit clearing is just one of the things you work on at Informal Systems. What other things are you working on?

We’re also working on other local monetary instruments, like vouchers and mutual credit. I’m not the top expert on this – I’m working with people like Paolo Dini and Guiseppe Littera, who used to work at Sardex, which I think is the second biggest mutual credit network that exists – I think that only the WIR Bank is Switzerland is bigger. What we’re working towards is marrying MOS / credit clearing (liquidity-saving) with what we call liquidity sources. This can be a lot of things. The simplest liquidity source would be a trust line between you and me. So, I trust you to return £100 to me within a set time, so I can provide liquidity to you. This new liquidity does its magic via the multiplier effect of the network. It’s the risk management of the liquidity provision that is usually costly. But in the case of this trust line, the risk is contained between the two members who decide to do this. It can’t spread further (this is the opposite of what happens with the banking system, where risk is socialised. What that means is that profit is privatised, and losses are socialised).

To then take it a step further, if there is a group of businesses that work / trade closely with each other, and they decide that they want to provide liquidity to the system by trusting each other, they can create a mutual credit club. It can be small (3-20 members) – you don’t need thousands of members to provide liquidity. In this case, the risk actually is socialised, but it’s contained within this small group. All the members of the group have agreed to be in it, and the overall MOS network provides a risk-reduction mechanism for all members, including liquidity providers.

You’ve said that in Slovenia, a pure MOS network, participating businesses can clear 10-20% of their obligations. What happens to this figure if you introduce a means of payment / liquidity source like mutual credit?

The amount of liquidity required to clear all debts can be measured. If all businesses in a net negative position (has more debts than credits) has access to liquidity that covers their negative position, then the solution is easy – everyone can clear their debts. Usually though, not all participants have access to this much liquidity. But being in a MOS network maximises the debt-reducing effect of any available liquidity. In the normal economy, outside of MOS / credit clearing networks, there is no way to achieve the optimum solution.

So it sounds like a game-changer. Having a credit clearing network can take you so far, but having liquidity sources and a knowledge of the local economy within communities that are enabled to prioritise their economic outcomes is completely transformative.

I completely agree. This is exactly what we’re trying to do. Our long-term objective is to provide tools to everyone who wants to use them, to create a resilient, well-managed monetary system that’s integrated into the rest of the economy. We don’t want to build isolated systems.

We’ve talked about the strong multiplier effect by including a means of payment like mutual credit – combining it with MOS / credit clearing. Your results come from computer models, but there is no empirical evidence from existing communities combining MOS with mutual credit / a liquidity source allowing most obligations to be met without money. There are no real-world examples of this having happened yet – is that right?

That’s correct when it comes to communities. But actually, this is happening every day within networks of financial institutions. MOS is what the finance industry calls liquidity-saving. Most people don’t know (not even bankers) is that at any moment, there isn’t enough money to cover all transactions in the economy. There are always payment queues and deferred payments. These simple methods can’t support the modern economy – it causes gridlock that is unresolvable using only these methods. So the payment system has to use MOS to be able to work. This is used extensively – 10 seconds of payment queueing, followed by 15 seconds of MOS / credit clearing. Without this shifting of modes, the real-time settlement system wouldn’t work. Banks would be forced to issue more money – but banks already issue too much money. Issuing even more to support the payments system isn’t really an option.

So, these systems are used all the time, but they’re not used to benefit ordinary people. What we’re doing is trying to bring these obvious and essential benefits (without which the banking system wouldn’t work) to ordinary people.

So there really is plenty of real-world experience in managing an operating these systems, but it’s not something that most people are aware of. I know that you’ve done research / computational models into what happens when you introduce liquidity sources / mutual credit into a credit clearing network. I read your paper from 2021, and I think the figures you came up with were that a participant in a credit clearing network might expect a 25% reduction in the need for cash, and then a further 25% from the use of mutual credit. Could you talk a bit more about that?

Yes, those are the figures, but there were restrictions – in that the participants wanted to be part of a credit clearing network, and the mutual credit system was designed responsibly. We wanted to be conservative – not to go for a theoretical maximum. We set up the experimental mutual credit system using the same criteria used in Sardex – i.e. the maximum credit a firm can get does not exceed 10% of annual revenue. If you relaxed this rule, and provided credit covering more than 10% of annual revenue, there would be more liquidity and you would clear more. But we didn’t want to provide unrealistic results.

I think we’re rapidly approaching a point where we can point to real-world examples. What developments are you most excited by?

I’m most excited by the fact that interest in these ideas is growing everywhere. There are many different types of projects growing around the world, using different models, under different conditions, that provide different challenges, which is very interesting and exciting. I don’t see the differences as a problem, but something that makes my work more interesting.

It would be too easy if you could solve the entire world’s problems in one go.

Yes!

How can people follow or get involved with your work?

The best way is to go to https://cofi.informal.systems/ – there’s lots of key information there, and we’ve started a blog. We’re trying to make all this as accessible as possible. We’ll announce there when we have new products that are ready to try. We want to help communities where there is a trusted local organisation that is actively involved in creating networks, but needs technical and implementation support. We’re also looking at crypto – although there have been some bad examples, and an idea that there can be a ‘crypto coin to save the world’ as well as a lot of speculative behaviour. We’re not aiming at those kinds of people, but we see blockchain and cryptographic tools as potentially very useful, for security and privacy.