We can’t build a commons economy with a capitalist money system. It will block us at every turn. But to build a new money system, first we have to understand the nature of money. Matthew Slater explains. Matthew is the author of the Credit Commons Protocol and white paper, and will be appearing at the Festival of Commoning in Stroud in September.

Amongst my environmentalist friends, one of their favourite novels of recent times is ‘Ministry for the Future’. In the book, the author Kim Stanley Robinson shocks us with how abruptly climate change might unfold. He also describes a policy response which seems unusually bold – the creation of a new currency that is linked to reducing carbon emissions. As an expert in alternative currencies, I was delighted that popular fiction turned some of my ecologically-minded friends on to the subject of money. I’d viewed environmentalism as failing to stem pollution and habitat destruction because the dominant ideology of growth, competition, and profit was seemingly out of their scope. But now more people are recognising that economics and monetary systems have a key role in that process, many falter at the complexity of the subject. Without a better understanding of how money systems operate and drive ecological destruction, inequality and other ills, environmentalists can only propose sticking-plaster solutions. In this short essay, I will explain some common misconceptions, before giving my view on how we can respond to the deeply unhelpful role of monetary systems in the current metacrisis.

The narrative I am hearing from some environmentalists, including those with significant online followings, goes something like this: Fiat money comes from nothing and because it is not backed its issuance is unconstrained. When there is more money than sustainable resources that leads us to overconsume. If money were backed by natural resources, we would value those resources more and consume less. Therefore we should lobby the government for more ecological money. This might sound intuitively appealing, but I’m going to explain why these are dangerous half truths – and point to a more helpful understanding.

To help explain my analysis, I will sometimes refer to the ‘Carbon Coin’ or Global Carbon Reward’ (GCR) showcased in the ‘Ministry for the Future’ novel. In the story, Carbon Coins are like globally standardised carbon offsets, issued to companies and projects which prove they have avoided carbon emissions. They can be traded freely until they end up on corporate balance sheets, proving that the corporation has financed official ecological regeneration, and reframing that contribution as an asset rather than a liability.

‘Fiat money comes from nothing’

The idea of something coming from nothing is a linguistic paradox, so we have to understand what is actually happening.

First of all, lets try to be clear where the dictionary, the law, and the economists are vague, by explaining what fiat money is, and what constrains its issuance. Fiat money means the notes and coins created by the government. For the sake of argument, I will concede that the government creates money out of nothing.

What uninformed commentators miss is that this public fiat money is only about 3% of all money. The other 97 is private money, issued by private banks, and the difference is significant.

On the government’s balance sheet, cash is a debt (a promise to pay the bearer on demand), but in practice it is not a debt. There may be an ontological problem here because the government debt IS money (at least according to the government, whose job it is to define money). That’s why if you take a bank note to the Bank of England and demand to be paid, they will simply exchange your bank note for a similar one.

But the bank’s promise to pay has to be honoured with government cash. You could say that this private money comes from nothing – it’s just like writing an IOU, but it also returns to nothing when the IOU is redeemed. In the same way an electron and a positron come from nothing, but they also cancel each other out when they meet. This is a perfectly acceptable way to issue a medium of exchange, by the way.

Carbon Coins also come from nothing – they would be just a number on a blockchain. There’s actually no problem with money coming ‘from nothing’ unless you insist that money is a asset in its own right, and not a balance sheet relationship with a corresponding liability.

‘Money should be backed by something’

What does ‘backed’ mean and why might money need to be backed? This gets right to the heart of monetary theory. Is money a commodity which facilitates marketplace exchange, or is money a relationship between creditors and debtors? If money is a commodity made of paper that presents very serious questions about what a commodity that you cannot consume is and where its value comes from. Those paradoxes go away if the money is actually a warehouse receipt for a real commodity that you can cash in at any time. But this happens very rarely in history. For as long as banks have existed, the word ‘backed’ only meant ‘partially backed’. The bank owns only enough of the backing commodity to meet the demand for withdrawals.

But backed monies also have awkward constraints. The value of money should be stable, yet when it is backed, the value fluctuates with the value of the backing commodity. Worse, there’s no reason why the quantity of commodity available should be equal to the quantity of money needed. Monetising a commodity increases the demand for that commodity and pushes the price up, perhaps by many multiples, distorting the market. Then the government has to manage that commodity to keep the money functional. And then if the economy needs more money, more of that commodity has to be warehoused.

I’m not sure that backed money is ever really needed. The state guarantees the bank money and if the state failed then there would probably be no way to redeem the money. In olden times traders might convert state money to bullion for foreign trade but the world doesn’t work that way any more.

Carbon coin isn’t backed, nor it is redeemable for anything, nor is it intended for use as a medium of exchange. It’s value is supposed to derive from the propensity of people and organisations to hold it, as a public recognition that they are supporting ecological regeneration. Governments could mandate this, much as normal money derives value from its ability to pay taxes and keep people out of jail.

‘There are no effective constraints on issuing money’

If this were true would we not have infinite money? It would be better to say that the quantity of money issued, and the directions in which it is issued, are intended to serve elites. They issue too much to themselves and not enough to the real economy. But let’s consider what the constraints are.

For public fiat cash money, the government creates as much as it thinks the economy needs for small transactions, stashing under the bed, and money laundering (NB 500EUR notes were discontinued in 2019). It has no incentive to issue more cash than the economy needs.

Constraints on bank issuance of money is a political hot potato. When a bank issues a ‘promise to pay cash’, that means it must ensure there is enough cash in its branches to meet demand for withdrawal. So banks are very good at estimating how much cash we need and dissuading us from withdrawing it. If even one person is unable to withdraw cash, the bank is technically bankrupt. So the amount of cash in circulation and the public’s propensity to hold cash do limit the amount of credit banks can create.

Carbon Coin is also constrained, but the mechanism is very different. Note that it is not a promise of anything but more like a receipt or proof of something. It can be issued only when the UN body determines that some carbon has been locked up for at least 100 years. From an ecological perspective the quantity of Carbon Coins should be as large as possible because it means that carbon is being locked up. However, the people holding Carbon Coin might prefer that fewer are issued if it means that the market price is higher. This looks to me like a mis-alignment of incentives.

‘When there is more money than sustainable resources that leads us to overconsume’

This is very contested in economics. Does the quantity of money/debt drive consumption or does the intention to consume drive the creation of new money/debt?

It is certainly true that if poor people have money they are likely to spend more, but richer people, whose needs and desires are more sated, spend less of their surplus on consumption and are more likey to buy financial products, pay off debt, or simply save the money.

Some excess money is not spent but saved or used to pay off debt. If the money is really in excess, then it will cause inflation and so it won’t be in excess for long.

Carbon Coin isn’t intended to affect consumption directly. It would displace money parked in savings accounts. It would create a helpful separation between money for circulation and money for saving, which would be a welcome simplification for monetary policy makers!

‘If money were backed by natural resources, we would value those resource more and consume less’

Again it sounds very sensible, but what does it actually mean? It probably intends that money should be 100% backed by resources that we monetise in order to value more highly – such as rare earth metals; or by resources that we want to preserve, such as wilderness or ecologically regenerative projects.

But I explained above that the backing commodity must be kept available for redemption, and that means it is not available for industrial use. So if policy makers wanted the economy to grow, they would have to lock up more rare earth metals; and if there was a shortage of those materials for the economy, they could only be made available by diminishing the money supply.

Now imagine that money is backed by ecological regeneration projects (e.g. planting trees) and there is a financial crisis. As demand for money goes down, the economy no longer wants those projects – they are worth more if the trees are chipped and sold for biofuel.

Carbon Coin doesn’t claim to be backed, but it can always be converted to money – firstly through the market which matches buyers and sellers, or if demand fails for any reason, the design says that central banks would guarantee to buy them at a minimum price. That means it is literally backed by central banks, like normal money.

So the notion of backing by natural resources doesn’t make much sense, at least to me. What makes more sense to me is using promises of energy as a medium of exchange and store of value. But that’s a subject for another article.

Finally I want to address the ultimate conceit, rarely considered, which is that:

‘Money is a legal instrument and can be improved through the democratic process’

My study and reflections on money over the years have led me to believe that the omnicidal money system is just a symptom of a deeper problem: the gangsters who run the economy and depend on money to project power and poverty. I believe that national and international monetary systems are not levers for us, ordinary folk, to change the balance of power.

It seems to me that the money system isn’t a static thing like a law waiting to be changed, but is already a scrum of power-brokers using vast wealth, propaganda, armies, criminal networks etc. to out-manoeuvre one another. Consider the ways that the money system has been mutating just this decade:

- the increasing use and forms of quantitative easing

- the eradication of cash and improvement of real-time settlement technologies

- debt crisis in the dollar and diversification from global dollar reserves

- regional (BRICS) alternatives to SWIFT clearing

- the growth of stablecoins

- tightening and relaxing of rules around reserve requirements

- growing ease of making international payments and holding money in many currencies

Like many aspects of our ‘liberal democracies’, there is no place at the negotiating table for the public, however strongly we may feel about it. These days I think that the mindset of systemic interventions diverts our attention from a deeper root of the problem, which is the people who build and manage the system. In other words, it’s not really a design problem but it always was, and still is, a class struggle.

Carbon Coin, as a systemic intervention, seems quite well conceived. I would say the same of Bitcoin, microcredit, Cap & Trade and many other good, even revolutionary ideas which found mainstream adoption. But in the process of implementation by experts, lawyers, entrepreneurs, financiers, management consultants and regulators, all of these ideas were severely diluted and arguably served those elites who controlled them more than the intended beneficiaries. That’s why ultimately I’m pessimistic about grand, top-down schemes like Global Carbon Rewards; rather, I put my energy and passion into creating financial instruments that people and communities can design and own.

That’s what I’ll be talking about at the Festival of Commoning in Stroud this September.

Conclusion

The money system has helped some human societies thrive, both by creating wealth and extracting it from others, but ultimately it has internal drivers that are not compatible with human thriving, equality, or sustainability.

I hope I’ve shown how statements about the money system that seem self evident or common-sensical are often unhelpful, if not completely wrong. It’s not surprising that many people struggle to be precise on this topic because it has so many conflicting narratives and overlapping vocabularies.

A better monetary system is a necessary part of a better economy, but the powerful are only interested in improving the system to enrich themselves. That system is breaking down and increasingly contested and has no capacity to include new ideas and values. Perhaps the best you and I can do towards a better system is to stop believing in the current one, to withdraw from it (to a greater or lesser extent), and create new, gangster-free informal economic contexts. Small, closed communities doing production, consumption, savings, investment, insurance could provide some insulation from an ever more precarious financial system, and counter the money trauma we all inherit from it.

As the global economy withdraws, withers and serves fewer and fewer people, it leaves new spaces for alternatives to emerge, as explained by Professor Jem Bendell recently

I actually agree with the environmentalists that it’s past time that the money system takes limits to growth into account. Even though narratives about money being disconnected from nature have a compelling feel to them, they might not be helpful in shaping useful initiatives. Rather, money design is not subject to democratic accountability, and therefore isn’t serving the demos, economically or environmentally.

6 Comments

As Matthew says, “…communities doing production, consumption, savings, investment, insurance could provide some insulation from an ever more precarious financial system, and counter the money trauma we all inherit from it.” True enough. If we, in our various communities, are to regain our power and independence, we must also create local liquidity, i.e, ways of paying each other that are “home-grown” and independent of banks and national governments. I explain all that in my new revised, Chapter 16—The Role of Credit Clearing in Regional Economic Development at https://beyondmoney.net/wp-content/uploads/2025/07/ch16_regionalecondev-final.pdf. This is the way we reclaim the credit commons.

Cheers Tom. Spoke with Tom at Local Loop Merseyside today – https://localloop-merseyside.co.uk. They’re hoping to launch the UK’s first city-wide clearing network this year, and are already talking with other cities to do the same when there’s proof of concept. Fingers crossed.

PS – I read your ‘End of Money’ in 2011, wrote an article that caught Tom’s attention, and he came in and worked with Dil et al to set up Local Loop Merseyside. So if it works, you could say that it’s ultimately down to you. So keep writing – you don’t know who you might be reaching!

(everyone – please do use the link Tom provided to the online, updated version of his book – it’s a gold mine).

I’m happy to see that Local Loop Merseyside is making progress in organizing local businesses and getting support from various community entities. Their website does not make clear if they plan to clear by finding loops for offsetting invoices or if they will be creating independent liquidity by allocating credit lines to participant members.

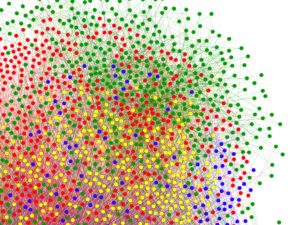

Tom – as far as I know – clearing via loops / offsetting is their main activity, but with liquidity injection for clearing ‘chains’ if they cant find loops (also ‘fans’ I think – but not too sure about that). Also, their software generates graphs that show dense clusters of trading activity – and they can offer mutual credit to those clusters.

Hi Tom,

You’re right that the Local Loop Merseyside website doesn’t say much about the mechanics – we’ve learned (the hard way) that this is a very bad marketing strategy. Articulating our intended customers’ situation and pain points in their own terms, and the outcomes we can offer, generates much more interest and understanding. We’ve still got a way to go with this, but at the end of the day it will be ‘show not tell’ that wins most people over, and so the number one priority is a successful launch.

As Dave says, the roadmap for mechanisms is loop clearing/offsetting of invoices, followed by fiat liquidity injection (‘fan clearing’ being our current non-technical term for this), and then endogenous liquidity (mutual credit and use-credit obligations) for the subsets of the network/club which meet the very restrictive conditions under which these are viable.

Federation (via the Credit Commons Protocol) of the small groups that can sustain endogenous credit will help adoption to scale somewhat (and also reduce the need for allocation and management of credit lines by us or any other centralised service provider), but I suspect that real-economy network structures will still impose severe constrains.

Thankfully, it should only require a relatively small amount of endogenous credit to substantially displace fiat when performing liquidity injection, and so even parts of the economy that cannot sustain their own credit will be able to start decoupling.