Where does money come from? A bit of history

Here’s a story. Only a minority understand this story (although I think that minority is growing), which is surprising because it has enormous importance for the way the world works. It’s a brief overview, and so it necessarily lacks detail, but it’s a true story in essence.

Step One

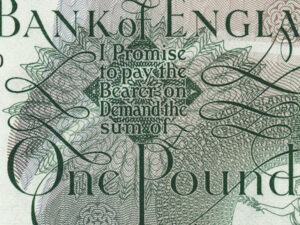

In the late Middle Ages, goldsmiths have fortified buildings to store their gold. Wealthy people deposit their gold, silver and jewels in the goldsmiths’ vaults for safekeeping, for a fee. In exchange, they get signed, sealed ‘promissory’ notes from the goldsmiths with the words ‘I promise to pay the bearer……’, and paper money is born.

Step Two

The goldsmiths notice that people very rarely withdraw their gold and jewels. Why would they? They have the paper notes instead, and their valuables are safe. So they start to hand out promissory notes as loans, at interest. Soon there is many, many times more money on loan than exists in vaults anywhere and the goldsmiths start to become extraordinarily wealthy banking dynasties. People recognise that their money is still safe in the goldsmiths’ vaults, but that the goldsmiths are making money from their money. They demand a cut, and instead of depositors having to pay the goldsmiths, the goldsmiths start to pay depositors for ‘use’ of their money to make money, and modern banking is born.

Step Three

The monarchs of Europe begin to worry about the wealth of the bankers, and about the stability of the new economy. Banks run the risk of collapse if too many people try to withdraw their money at the same time; worse, the European economy is now dependent on bank loans, especially to fund overseas expeditions; and even worse (for them), royal power might be threatened by the runaway wealth of the bankers. States start to regulate the banks, and in the 17th century, central banks are established to hold their bullion reserves, and restrict the amount of money they can lend out via the ‘fractional reserve‘ system – so called because banks only actually possess a fraction of the money they lend out.

Step Four

By the 20th century, the fractional reserve system is the standard form of banking worldwide. The reserve requirement differs between countries, but an average is around 10%. If the rate in a country is 10%, or 10:1, and if someone founds a bank by depositing a $10,000 reserve at the central bank, they can then loan out ten times that amount to their first customer. That first customer can then take his or her $100,000 to buy something, and the seller can then deposit that $100,000 in their bank. The seller’s bank then considers this ‘real’ money (although it was originally a loan) and they can keep $9,091 of it in reserve and lend out $90,910 (i.e. ten times the amount kept in reserve). This new loan gets deposited in another bank, and the process continues until, eventually, over $1 million is created from the original reserve deposit of $10,000.

This means that if you take out a loan, including a mortgage, the bank will bring the money into existence by typing numbers into a computer, then you are in debt to them, with interest, for money they didn’t have. Genius.

Step Five

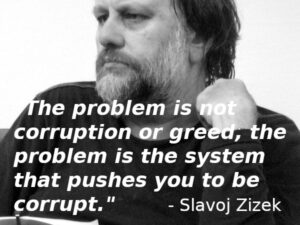

The fractional reserve system concentrates wealth and power at the top of the corporate and financial sector, and prevents the economy from stabilising (resulting in ecological damage). But the money men aren’t satisfied – they develop a bewildering array of credit default swaps, hedge funds, currency speculation, derivatives and other forms of gambling until the heart of the global economy becomes, in effect, a giant casino. But it still isn’t enough for them, and by the 1980s their political donations and lobbying activity is so huge that they’re able to remove most of the remaining regulations limiting their money-making activities.

Step Six

There’s an explosion in the financial sector. Foreign exchange transactions alone now total over 20 times the amount generated by the ‘real’ economy – i.e. trade in commodities and services. Offshore financial havens and the issuing of credit cards by chain stores make a mockery of any kind of financial control, and funding of politicians and parties by the financial and corporate sector makes a mockery of democracy, but ensures that in good times, banks will make enormous profits and in bad times, taxpayers will bail them out.

Step Seven

You decide. Ancient Rome was an empire built by the work of slaves for the benefit of a tiny minority, and nowadays the corporate / financial empire is the same. The vast majority of the world live in poor countries and either work in or service corporate factories or plantations. They are, in effect, slaves, paid just enough to survive, with no escape. In the West we are mortgage and wage slaves too, but with ‘bread and circuses’ – fast food, sport, shopping and celebrity gossip – to distract us from the reality of the situation. But Rome fell in the end, and the unsustainable nature of this empire will ensure that it will fall too. Do you want to continue to mortgage yourself to them, work for them, shop in their supermarkets, bank with them, get into debt with them to buy their consumer goods and follow their fashions? Or do you want to stand up and say ‘I’m Spartacus’?

—————————————————————————————–

NB: update – there is no longer a fractional reserve system in the UK. See here.

The views expressed in our blog are those of the author and not necessarily lowimpact.org's

7 Comments

-

1me-again February 5th, 2016

As you say, it’s all funny-money in the end. This leads to the bit that very few people understand, including the author of this post: The fabulously rich aren’t *really* fabulously rich, it’s all numbers in a bank account. They can’t actually take that cash out of the bank and spend it, because the bank doesn’t have the money. Sure they have lifestyles that other people are envious of, but the reality is that far far far more money is spent on keeping ordinary people in comparative luxury without working including the unemployed, the disabled and pensioners. And before you get on your high horse shouting that the way disabled people and pensioners are treated is a crying shame, go and take a look in Nepal, Afghanistan, India, Peru, Bolivia etc. etc. and see how they’re treated there. Don’t get me wrong, I’m not a fan of capitalism as it is, and I agree that too much wealth is going to the wealthy at the moment, but you’re sounding a bit like the rebels in “Life Of Brian”: “What have the Romans ever done for us? [except the roads, the aquaducts, protection from enemies … etc. etc. ]”. If you don’t like capitalism it’s still possible in this country to live a cashless existence: You can still hunt and gather on the seashore and in the sea, and there are plenty of places you can build a shack out of recycled bits and pieces in caves in old quarries on the coast. However, if you deny yourself access to the National Health System (a product of capitalism) your life expectancy will reduce to 40 years (less for a woman), and half your children will die before they become adults. Also, if you deny your children an education (another product of capitalism) they will be sentenced to a life exactly like yours (if they survive long enough) because that’s all they will ever know. People buy into capitalism because it serves them. Soviet Communism was just the same except the “funny money” was all owned by “The State”. People still managed to have lifestyles that included private jets, villas in resorts etc. etc., it was just that the politburo decided who those people were rather than a random series of historical events. Also the politburo decided exactly what got manufactured so loads of stuff got made that nobody wanted, and a lot of stuff that people wanted never got made.

-

2Dave Darby February 5th, 2016

The problem is that it can’t continue – http://lowimpactorg.wpengine.com/lowimpact-topic/the-nature-problem/

The effect that corporate capitalism has on democracy is much more worrying to me than financial inequality – http://lowimpactorg.wpengine.com/lowimpact-topic/the-democracy-problem/

Plus I’ve made it clear many times that this site is not advocating a soviet-style solution – http://lowimpactorg.wpengine.com/review-why-marx-was-right-eagleton/

I’m inviting discussion as to what a sustainable, non-corporate system might look like.

-

3johnhson February 5th, 2016

The thing is, what will follow the fall of this empire? Rome’s power declined over a period of centuries as the cost of maintaining the empire grew and the size became unmanageable for the transport and communications technology of the time. When the legions left Britain, which was an integrated part of the empire and enjoying a relatively high standard of living – the door was open to invasion and power struggles. AKA the Dark Ages

We’ve seen the effect of just removing a power structure with no acceptable replacement. The death of Tito and the dissolution of Yugoslavia was followed by a blood bath, the collapse of the soviet union went better (Poland, Latvia etc) but Russia has ended up with a dictatorship as have some of the smaller, eastern republics.

The removal of Saddam who may have been an evil dictator has hardly improved the lot of the average Iraqi.

Rejection of the current system could go awfully wrong – Cambodia’s rejection of modern society resulted in the killing fields. The ISIS extremists are another example of rejecting the globalised world.

I don’t mind saying ‘I am Spartacus’ but I don’t want to be crucified!

-

4Dave Darby February 5th, 2016

‘I don’t mind saying ‘I am Spartacus’ but I don’t want to be crucified!’ – yes, I know what you mean. Me neither.

I tend to have two kinds of discussions about this – the first is with people who say (more-or-less): I’m secure – I have a roof over my head, I eat well, I have a flat-screen TV (etc.), so I don’t want to rock the boat.

The problem is that a) it’s not sustainable – it damages ecology too much, and b) their security and comfort is built on the backs of hundreds of millions of plantation workers and sweatshop workers in poor countries – it’s effectively slavery. Not good.

The second kind of conversation is about attacking the system whether we have an alternative or not – the premise being that this system is going to make us extinct if we don’t stop it – we can work out what to replace it with later. But the longer we leave it, the stronger this system gets and the less likely we are to be able to replace it.

I’m with you on this one.

I’d much rather talk about building alternatives.

Lowimpact.org is, so far, all about individual change – http://lowimpactorg.wpengine.com/topics-2/

But we’ve started to talk about economic change – http://lowimpactorg.wpengine.com/move-your-money/ – which put simply, is about building ‘the commons’. We’ll be doing more on this later this year.

At some point, we need to talk about building a new political system that doesn’t allow access to corporate money or influence. This system allows those things to happen very easily – rolls out the red carpet, you could say.

I certainly have some ideas, and welcome others.

-

5Nane February 5th, 2016

What if our system were based on the Love Of All Humanity? Wouldn’t that be something special? Unfortunately, we’re going to have to wait until everyone evolves into that. In the meantime, we could … just start supporting each other

-

6mikeceocker February 5th, 2016

You forget the origins of money via the barter system, a skin traded for two barrels then for 3 sheafs of wheat then 4 quarts of port until it became too complex, so other standards were used, gold silver et al and then the promise to pay, hence money.

As for living in a cashless society, its flip to imagine doing it but until you try it its not realistic,I know I tried it for a year, the most difficult thing is leaving the comfort of the old life behind, not the actual physical comfort but thatof the psyche, leaving your tv and mobile phone and computer and all the other stuff behind, its not until, psychologically, we don’t have them but the need to have them, modern man is too conditioned in this modern technological age to return to hunter-gatherer. Again its not until you try it, you still need money [or a barter system] to buy seed or a fishing licence or bait [depending on season] or a knife to skin your rabbit and a potto cook it and matches to light the fire. As much as we like to think we can go out and purchase a flint, for free or dig it out of the ground with our free shovel and cure our rabbit skins to make a coat to keep us warm!

The society we live is one which, like past empires will have its day because money is the root of all evil, the evil perpetuated by the 1% who already have 90% of the wealth until us poor people have no more money and rebel, money is just a piece of paper. When the Detroit motor industry collapsed, the people tore down the factories and ripped up the tarmac and began to grow crops.We are beginning to see the collapse of the greatest modern empire, China, with their disenfranchised populace rerooted from their natural habitats to work in factories producing plastic, grow rice when the system collapses, when inflation and the supply switches to India or Africa [where labour costs are lower] and the man says my grandfather grew rice but he never taught me because I was busy earning money to buy rice. In India now, subsistence farmers have their land seized to build shopping malls and factories building and selling more technology. The modern system will fail for one simple reason, food, or the lack of it because we can’t eat plastic!

-

7johnhson February 5th, 2016

I had a few friends who lived cashless until we all got fed up of them not buying their round ? But you’re right in that our system is based on exchange tokens we call money and we can’t live in a system based on that without it.

Having spent a lot of time researching, my prediction is the food crisis will be with us sometime between 2030 and 2050. We can’t eat plastic but I suspect the bulk of our diet in 2050 will come from our gardens or vats in factory units.

How has the 2008 financial crash affected the wealth of the rich and the poor, and what can we do about it?

How has the 2008 financial crash affected the wealth of the rich and the poor, and what can we do about it?

Where does money really come from? (erratum: there is no fractional reserve system in the UK)

Where does money really come from? (erratum: there is no fractional reserve system in the UK)

Where do banks get the money for mortgages from?

Where do banks get the money for mortgages from?

Why international investors (i.e. ‘the 1%’) couldn’t care less about politics

Why international investors (i.e. ‘the 1%’) couldn’t care less about politics

What’s the relative value of the world’s gold, Bitcoins, banknotes, derivatives, stocks & shares, property etc. See this incredible visualisation

What’s the relative value of the world’s gold, Bitcoins, banknotes, derivatives, stocks & shares, property etc. See this incredible visualisation

Low-impact money

Low-impact money

System change

System change

The 'democracy problem'

The 'democracy problem'