Today I’m talking with Shaila Agha of Grassroots Economics and the Sarafu Network about ‘chamas’ and mutual credit, and how they’re changing Africa.

Really nice to talk with you Shaila.

Thank you – happy to be here.

I recently interviewed the founder of Grassroots Economics, Will Ruddick, so I’ll link to that interview in the description. But if I say that the Sarafu Network is a mutual credit network that allows trading without conventional money, that includes 50,000 households across Kenya and did $3 million worth of trade last year – how’s that for a brief description?

Yeah, actually we’re up to 52,000, and last month we had 4200 new users registered.

What kind of traders are they?

Mostly food / agricultural produce. Food sellers and farmers.

And what’s your role there?

I’m the incoming director, dealing with business development and funding.

And how well is it doing – what does the future hold?

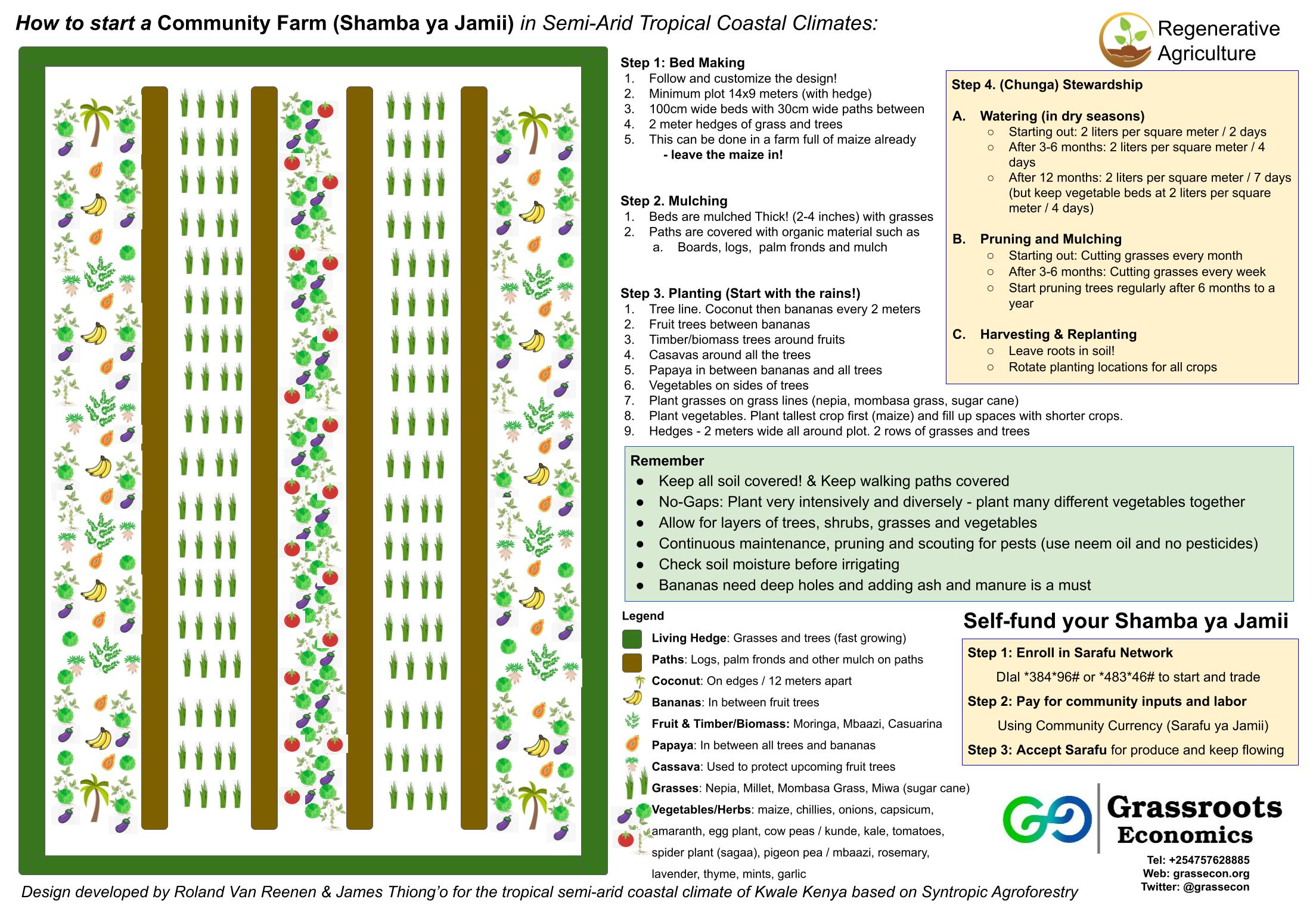

It’s growing fast. We’re developing new businesses, like pressing coconut oil. Also ‘syntropic farming’ (see poster below) – a system of farming that includes trees, vegetables and grasses, and a lot of mulching and a lot less water than traditional farming. The trees form a barrier – monkeys are a pest in Kenya. Then there are different rows with grasses and other plants. We provide training in mulching and water pans as well. Kenya is arid / semi-arid, so we need resilience against times of drought. So we train people in that. All these services are then paid for using Sarafu, and people accept the Sarafu because they know they’ll be able to buy produce with it.

Yes – Grassroots Economics isn’t just about mutual credit is it? It’s about starting community businesses, and especially agriculture – community farms.

Yes, it creates this circular economy. There’s poverty-induced hunger in Kenya during droughts. This doesn’t make sense, because we live in such a resource-rich country. There are so many unemployed youth too, but I feel like we’re addressing this, because people don’t have the money to buy what they need, so if we can provide this supplementary currency, then they’re able to get agricultural produce with it (which combats both unemployment and hunger).

What do you think the Sarafu Network could achieve in future?

In Kenya we’d love to scale nation-wide. One of the barriers is the expense of the Telcos – telecommunications. The network uses texting – and all texts are paid for by Grassroots Economics. That’s doable with 52k people, but what’s going to happen when it’s a million people? That will be too expensive. Also, government acceptability – wouldn’t it be great to pay for parking, or other government fees with it as well? At the moment, only people with money can access government services, whereas if they could use Sarafu, there’s a huge number of unbanked people who could participate in the economy.

Have you had conversations with the government?

Local government are on board. There’s been devolution recently, so now each county has its own administration, so there’s more opportunities to reach the more open, tech-savvy counties. For example Nairobi now has its own USSD code with which you can pay for parking and other services. So they already have a digital payment system. We just have to move away from the idea that it’s for vulnerable households to the idea that it’s for everyone.

So I guess you can point to successes you’ve had when you’re talking to local governments. We’re trying to start clubs in the UK, but we don’t have any clubs up and running yet that we can point to.

It’s still a little difficult when talking with local government. I’m talking with the chiefs and the elders. They are the lowest level of government. They’re the ones who can see the changes on the ground. They know that some families didn’t have food, but now they’re empowered (by Sarafu) and they’re doing their own thing. They’re on board, and we use them as mediators when talking with government.

What contact do you have with development organisations? Instead of the big charities pumping money into developing countries, they could help develop mutual credit networks? Conventional money just leaks away eventually, and ends up in tax havens.

Yes, we’re in talks with an organisation to go to Cameroon and do some research on how scalable it might be – to do it nation-wide.

Cameroon? Is that the German government who are involved with that?

Yes. That’s GIZ (German development organisation). But all we need is a government, and telecoms company and an aid organisation coming together to say ‘let’s do this’. It’s relatively easy to do. We did have an accelerator workshop with the World Food Programme recently. They were really interested in our agriculture systems. We told them that we needed government support, and that they had the ear of the government, because they’re a huge donor. If they could talk to government and ask them to listen to us, maybe give us subsidies so that we can scale up.

I read that the German government was involved with setting up community currency schemes in Cameroon, but I didn’t know you were involved as well.

Right now we’re researching it. Doing a feasibility study into its viability. We need to know whether the people will accept it. (Shows paper sarafu money) – we need to be sure people will accept this for goods and services.

Just to be clear – you don’t use the paper money any more.

Yes, it’s all digital now – which is much better. You can’t steal it, no printing involved, less fraud etc. It’s a digital age – we needed to go digital.

What do you think the biggest barriers might be?

Government acceptance. If we had the government on board, we’d be light years ahead of where we are now. I think they’re a little bit wary, because blockchain technology isn’t easy. But our Capital Markets Authority is now working with three other blockchain companies, so they’re trying to understand, and they’re setting up regulatory sandboxes for these companies. We’re going to apply too. We need to get their ear, so that they understand what it’s about. In the past they’ve thought that these kinds of ideas were something to do with secession.

Yes, they thought Will was part of a secession movement, didn’t they – and he had a bit of jail time?

He did. And it wasn’t just him – it was the whole team. Luckily I wasn’t here then. They tried to say they were doing something fraudulent, but it was ridiculous.

It might have been a good thing in the long term – a bit of free publicity.

Absolutely. So the long term goal is to get the government on board, and even to be able to pay taxes in Sarafu. A lot of the Kenyan population is not taxed at all. So this could give people an opportunity to contribute back to the economy.

Tell us a bit about your background, and how you found the Sarafu network / Grassroots Economics.

As an undergraduate I studied finance and economics, and I got into banking and investment systems – this was during the 2007-8 financial crisis. I was working in Canada, and I could see the effects of the crash on ordinary people, but I was working with people who were hoarding lots of money, and didn’t really care if they lost millions. It didn’t make sense to me. I started getting interested in decentralised finance. I worked in the development sector, and for the UN. But the bureaucracy was so demotivating. So I started to study fintech, and disruptions in financial technologies. I found out about Bangla-pesa, and I studied it. I thought it was pretty cool. I met them at a conference in Nairobi, and I thought that this was the type of disruptive technology we need. Then last year when I moved to Kilifi, I discovered that Will’s office was walking distance from my house. I decided I needed to get involved.

I want to talk about chamas – very important in developing mutual credit networks in Kenya. first could you explain what a chama is?

They’re groups that started in the 80s, when Kenya was really in a cash crunch. They started off as women’s savings groups, but now they’re open to men as well. There are social bonds – family, church, work. They already know and trust each other. They meet up, and they have something called the ‘merry-go-round’ system. They all pay into a fund, and each time, one of the members takes the whole fund. So it’s a micro saving and micro lending scheme. Chamas are really great, and for Sarafu, they’ve been the best groups to work with.

Are they completely new, or has this sort of thing been around for a long time in Kenya?

Since the 80s. My mum’s involved in 4 chamas. I’m in 2. Everyone I know in Kenya is involved in a chama. It’s a thing that people do. It’s a way of getting a loan. Otherwise, access to credit is really expensive and difficult. Recently we’ve had aggressive campaigns by loan companies, but they don’t inform the public about their interest rates, which are ridiculously high. So at Sarafu, why we love chamas so much is that we just have to go in and give training. There’s already a self-governing group – a network of traders.

That’s such a gift.

Yes – we’re just liquidity providers. We just come in and say ‘here – trade!’

Oh my god, that’s exactly what we need everywhere. So they’re completely embedded in their communities?

Yes.

Were the chamas involved in the Sarafu network right from the beginning?

Some of them were. They’re always been there. It’s been a parallel development. We didn’t have to persuade – they started to use sarafu on their own. It’s great for them because they already have that trust system. Asking someone you don’t know to accept sarafu is one thing, but asking a fellow chama member is another. Actually, before sarafu, they were already doing it with goods and services – with vegetables, or bags of flour, sugar etc. Now with sarafu, they can use it outside the chama too.

I didn’t realise that virtually everyone in Kenya is involved with a chama. I thought it was a marginal thing.

No – it’s everywhere. I have a friend who works for the UN in Kenya, and they have a chama. They invest in land and apartments. My mum’s chama is with neighbours, and they bought land together. It’s a means of having credit with a negotiable interest rate – which is the biggest thing. People don’t have much faith in the banking system in Kenya. We’ve been pushed around. One morning you wake up and the interest rate has changed by 5%. Plus there are hidden fees. You sign up for a loan with 14% interest – which is already ridiculous in my opinion. A couple of years down the line, you realise you’re actually paying 22% because of these extra charges. So people decided: why don’t we just do it ourselves, without banks? Just loaning our own money to each other. So if one month you can’t pay, you just talk to the chama and negotiate. It’s less scary than going with a traditional bank or loan company.

Is there a national chama network, or are they all independent and separate?

They’re independent. We do have another thing you should look into. They’re called saccos. They’re chamas with set rules, and have larger numbers. I believe they have to have a banking licence too, because they’re dealing with larger numbers. Big companies have saccos for employees, the UN has a sacco for its employees. You have preferential interest rates, negotiable terms, and it’s a little less personal. They’re regulated by the Kenyan government (and you have to have regular employment – and show payslips). It’s more of a middle class thing – but the same idea.

Are you working with the saccos too?

Not yet. Although I think that should be the next step.

Have you come across any chamas that don’t like the idea of mutual credit?

No, they love it. I don’t know what your interest rates are like in the UK, but for us, getting a credit card is a disaster. In Kenya we don’t buy things on credit – only a niche population does that. Very few people have employment security.

Do you think the Sarafu network could have grown to the size it is without chamas?

Absolutely not.

That might be a problem for the UK – because we don’t have them! How can we get them?

It’s a different country with completely different issues. People like Sarafu in Kenya, but they wouldn’t use it as much independently than they do via their chama. Most transactions happen via the chamas, because there’s already that network. But in the UK you have different network – maybe networks of football supporters, or pubs. There are trust systems in pubs – some people have a tab at the bar, which they settle later on.

I’m not sure it’s that common these days, but I could be wrong because I live in London, where there’s less community.

Yes, London isn’t really like the rest of England.

We don’t have the kind of community cohesion that you have in Kenya. When I spoke with Will, he said forget Europe and North America – mutual credit is going to spread through Africa, Asia and Latin America first. That’s where the need is.

And also it’s where the word community still means something. Recently a neighbour lost a child, and I’ve never seen a funeral so big – the entire community turned out. The social connection and cohesion is more than it is in the West. People show up for other people a lot more.

Poster outlining the syntropic farming system (click on image for larger poster).

Poster outlining the syntropic farming system (click on image for larger poster).

We talked earlier about the Credit Commons. We now have the software to join mutual credit groups together. I spoke with Will about this – but it would be such a great thing to connect Europe and Africa – as well as the rest of the world. A small coffee shop in the UK could buy coffee directly from a small farmer in Kenya, via mutual credit, without all the middlemen. There’s no role for middlemen, or corporations, or banks – they’re totally unnecessary.

That’s the dream, really. Imagine setting up a zero waste company, or a fair trade company in Kenya. Why is it so hard? Because everything is imported. You need tin foil bags to put the coffee in – they have to be imported and you need money to get them. Same with the twisty ties for packaging etc. What if you could get all these zero waste and fair trade companies together to form a network and trade in mutual credit? Then they could save their fiat currency for where there’s no alternative, and use mutual credit to import things they need to trade.

Then maybe you could help start packaging companies in Kenya rather than having to import everything.

Absolutely.

Do you think that helping small business to survive, using mutual credit could save a lot of people from sweatshop work or plantation work, which is more-or-less slavery?

Yeah. I can tell you Dave, that people don’t choose to be in those working conditions. We have a big unemployment problem. Entrepreneurship is harder because access to credit is so expensive. Mutual credit builds so much resilience. It builds liquidity into society and allows people to follow their passions. It allows them to do what they really want to do. You give them the opportunity to use their resources. That’s empowerment.

It’s similar over here now. Lots of small businesses have gone under after the Covid lockdowns. In working-class towns, the only available work will be things like Amazon warehouses, which is terrible work. I think mutual credit can provide an alternative to that.

One of the field officers I talked with last week said that in his area there was drought and farmers were struggling. Women had to wait for their husbands, who were working in Nairobi, to send them money via M-Pesa – and there’s an M-Pesa system now where you can take out an overdraft on your account, but the interest rates are crippling. But people aren’t very financially literate, so they’re taking loans without really knowing the terms and conditions. Lots of vulnerable households are falling for it. But with Sarafu, we’ll call people to find out about their circumstances. We tell them that they can join a chama and get milk and agricultural produce via mutual credit. They get an intitial 100 bob, but after that’s gone, they can trade via the Sarafu network.

Did you say ‘bob’? The old English word for a shilling was a bob.

That’s exactly the same in Kenya! The field officer told me that he’s seen it with his own eyes. People used to eat rice just at Christmas, but with Sarafu they’re eating rice throughout the year. So there’s a qualitative change in people’s lives.

I saw the research – where food consumption goes up in areas that use mutual credit. I told you earlier that I was in Tanzania in the 90s, and I visited Ujamaa villages – where people work together, and have direct democracy. It feels to me that with the Sarafu Network, and chamas, staccos, and Ujamaa, that there are so many fantastic ideas coming out of Africa, that we have a lot to learn in Europe. We’ve lost a lot.

Yes. I think there’s some beauty in being ‘underdeveloped’. We have the opportunity to look to the West and to see what mistakes you’ve made, and hopefully not make them too. We’ve been able to take technology and make it better for a poor country. And necessity is the mother of invention. There are some brilliant ideas and brilliant minds coming out of Africa – we just haven’t been given the opportunity to shine. I truly believe that Africa is the new frontier.

I think it is. Shaila it’s been fantastic talking with you. Let’s keep in touch. If we can build mutual credit networks in the UK, I want us to make links with the Sarafu Network and other networks in Africa.

Definitely interested in the Credit Commons – so for sure.

Let’s keep in touch. I’ll let you know what we’re up to in the UK, and I’ll follow your development on your website too.

Thanks Dave – bye.

Highlights

- People don’t have much faith in the banking system in Kenya. So people decided: why don’t we just do it ourselves, without banks?

- The social connection and cohesion (in Africa) is more than it is in the West. People show up for other people a lot more.

- Mutual credit builds so much resilience. It builds liquidity into society and allows people to follow their passions. It allows them to do what they really want to do. You give them the opportunity to use their resources. That’s empowerment.

3 Comments

Do you need a quick long or short term loan with a relatively low interest rate as low as 3%? We offer new year loan, business loan, personal loan, home loan, auto loan,student loan, debt consolidation loan e.t.c. no matter your score, If yes contact us via email: [email protected]

Hello, Do you need a loan from The most trusted and reliable company

in the world? if yes then contact us now for we offer loan to all

categories of seekers be it companies or for staff usage. We offer

loan at 3% interest rate, Contact us via Whats app

[email protected]

LOAN SEEKERS APPLICATION FORM

******************************

1) Full Name:

2) Gender:

3) Loan Amount Needed:

4) Loan Duration:

5) Country:

6) Home Address:

7) Mobile Number:

?? Fax Number:

9) Occupation:

10) Monthly Income:

11) Salary Date:

12) Purpose of loan:

13) Where did you get our loan advertisement:

[email protected]

Are you searching for a very genuine loan at an affordable interest rate of 3% process and approved within 4 working days? Have you been turned down Constantly by your Banks and other financial institutions because of bad credit? Loans ranging from $5000 USD to $20,000,000 USD maximum LOANS for Developing business a competitive edge / business expansion. We are certified, trustworthy, reliable,efficient, Fast and dynamic for real estate and any kinds of business financing. Contact us for more details and information.

Thanks & Regard

Indiabulls Housing Finance Pvt Ltd

E-mail: [email protected]

Reply