Rotating savings & credit associations (ROSCAs) - introduction

Lowimpact.org is now archived. Topics are now curated by specialists on Growing the Commons. Here’s ROSCAs — rotating savings and credit associations on GtC.

“The poor man’s bank, where money is not idle for long but changes hands rapidly, satisfying both consumption and production needs” – F J A Bouman

What are ROSCAs?

They’re groups of individuals who agree to meet for a defined period to save together. Each member contributes a fixed amount to a common pool at regular intervals – maybe weekly or monthly. At each meeting, the entire pooled sum is given to one member, with the process rotating until every participant has received the lump sum once, after which they start again, or the ROSCA dissolves.

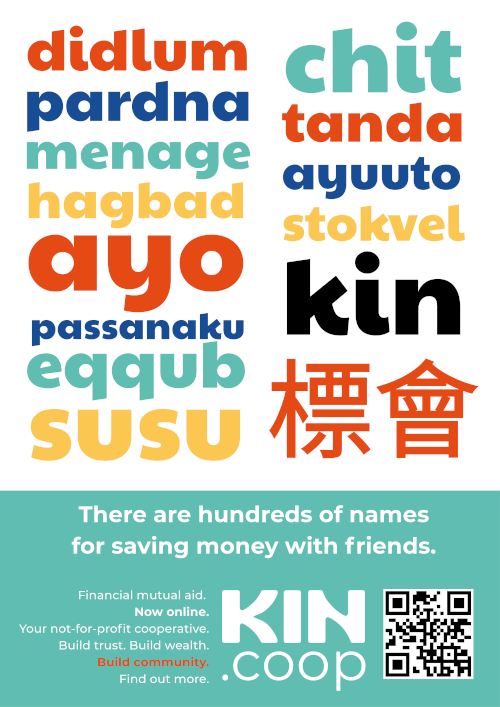

Some of the many different names for ROSCAs in different countries / communities.

‘Rotating savings and credit association’ is more of an academic term – they have different names in different communities, for example, Jamaican ‘pardna’ schemes, English ‘didlum’, Scottish ‘menage’, Punjabi ‘kitties’, Indian ‘chit funds’, East African ‘chamas‘, Somali ‘Hagbad’ and many more.

As an example, imagine a group of 10 friends or neighbours, each putting in £100 per month, and every month, one person will take the whole £1000 (maybe because they have an expensive event like a wedding coming up, or they need a new vehicle, they have an emergency to deal with, or a new business opportunity). This continues until everyone has taken the pot. The group might decide the order of people to take the pot, based on their circumstances, or they might do it by lottery.

History

They’re among the world’s oldest and most enduring informal financial systems. They’ve enabled millions of people – especially those excluded from formal banking – to save, access credit, and build community resilience. They rely on trust, social accountability, and community ties rather than legal contracts or banks.

Their history goes back thousands of years. They were documented in China around 200BCE, they exist all over the world, and are particularly common in sub-Saharan Africa. According to the World Bank, around 25% of people in sub-Saharan Africa report having used a savings club.

Savings clubs were the ‘seeds’ of the building societies (money was pooled for members to be able to buy houses) and quite possibly the entire co-operative movement. ‘Didlum’ groups started to appear for the same reasons that co-operative and mutual societies did – the hardships being experienced by working-class communities in the growing industrial cities of the early 19th century, with the poor laws and enclosures pushing people off the land, where they could have supported themselves. Savings clubs led to bulk-purchasing shops and then co-operative and mutual societies themselves.

When you look at modern large co-op movements like SEWA in India or Mondragon in the Basque Country, they really started to take off when they created a community bank. It was because of this pooling of community resources that they were able to invest in themselves, so that they could de-couple from the capitalist banking and shareholding model.

Variants

They’re extremely customisable, so they can function as anything from a shared fund among friends, all the way to a micro-credit union. The most common version is a small group of people with a rotating fund. Each person puts in a regular amount. In some groups everyone will put in the same amount every week; in others, the amount will change, or different people will put in different amounts. If no-one is in any great need, they might also decide that no-one takes the pot for a while, and it’s allowed to grow.

Some of the chit funds in India are extremely large, have their own offices, and have therefore come to be regulated more than others. They can include whole villages – but the larger they get, the harder it is to maintain trust among members. Fraudulent activity still happens very rarely (because the social cost is so high), but even less so where groups are smaller and social bonds stronger.

Statistically, they’re most commonly run and used by women.

There are no fees or interest involved, but sometimes, for example in the pardna variation, people might put in their monthly amount, with a little bit extra for the auntie who runs the scheme – but out of gratitude, not compulsion.

What are the benefits of ROSCAs?

Personal

ROSCAs serve multiple functions, including insurance and socializing, as well as economic support. They work well for people who find it difficult to save, to get bank loans, or to pay the high interest on payday loans.

They can help members start a business. And even in better-off communities, they can allow people to achieve things they wouldn’t have been able to achieve alone. For example, one of kin.coop’s co-founders (a migrant) was able to finance her law degree without a student loan when her community formed a hagbad (a Somali ROSCA), and she’s now a law professor.

They also work well for Muslims, as there’s no interest (usury) involved.

Environmental

Their big environmental benefit is that because there’s no interest or profit, there’s no growth imperative – in other words, they can work as part of a stable local community. Perpetual GDP growth is the real killer of the biosphere.

They can also help members to get solar panels, wood stoves, heat pumps etc.

Democracy / decentralising power away from corporations

ROSCAs do this directly, by taking business away from corporate banks. Providing things for ourselves in communities helps prevent extraction, decentralises power away from corporations (which makes it more difficult for them to corrupt democracy) and democratises work.

As mentioned above, they provided the seed for various mutual / commons movements. They can seed all kinds of mutual aid / commons institutions / community development in the future too.

Community / collapse preparation

ROSCAs can really help us to look after each other – they’re one of the best tools around for community and resilience building – and they work well in working-class communities.

If a financial collapse kills the banking sector, people can carry on pooling money in communities, and it can be done with notebooks and pens if necessary – or even in people’s heads. In dire circumstances, it’s the connections between people that are important. We could even stop using money altogether and move to mutual credit relationships, pooling goods and services for each other, rather than money, and accounting for it using digital or paper tools (or memory).

ROSCAs are one of a growing range of financial tools for a new, commons economy, including credit unions and building societies, and (moving towards systems that don’t need banks or money at all) credit clearing, mutual credit, use-credit obligations and the Credit Commons protocol. These financial tools can also connect with other community-based initiatives around assemblies and governance, housing, energy, food and other essentials. Things are developing very quickly, with more and more places for people to slot in.

What can I do?

ROSCAs are more difficult for Westerners to get their heads around, where community has been weakened, and people have organised their finances via individual relationships with corporate banks. It’s a much easier concept for people from the Global South, where communities are more intact.

Forming a ROSCA

- Identify potential members: gather a group of people you trust – family, friends, co-workers, or community members.

- Agree on terms: decide on the contribution amount, frequency of meetings, payout order, and duration of the ROSCA.

- Establish rules: set clear rules for participation, including how to handle missed payments or disputes.

- Choose an organizer: select a reliable person to coordinate meetings, collect contributions, and manage payouts.

- Maintain transparency: ensure all members are aware of transactions and decisions. Keep simple records.

- Monitor participation: encourage regular attendance and contributions. Review after 6 months.

There are apps / platforms that can help you get started, or to have online ROSCAs – but be very careful, because corporations will try to muscle in if they think there’s money to be made. But there’s absolutely no need for giant corporations to take a cut. Please, please, beware of extractive corporate / fintech startup versions. Avoid at all costs. We recommend co-ops like kin.coop.

Their app collects monthly payments and stores them in (co-operative) bank accounts, building societies or credit unions, so the funds accrue interest. The groups then decide what to do with the interest – which could go to help the community, or to charity.

This is breaking new ground, and will undoubtedly confuse regulators, just as peer-to-peer lending platforms did – but hopefully regulation will bring about the acknowledgment they deserve without removing their autonomy.

Co-ops like this can play the role of secondary co-ops, helping more local groups to form, develop and connect.

What’s working quite well is food-buying groups, who can save money by pooling funds to buy food in bulk together.

Further resources

- ROSCAs as an Islamic micro-finance vehicle

- Bank of England: resources from an exhibition about ‘pardner hand’ – ROSCA of the Windrush generation in the UK – including articles, interviews and free school resources

Specialist(s)

Thanks to Rob Callender of kin.coop for information.

The specialist(s) below will respond to queries on this topic. Please comment in the box at the bottom. of the page.

Rob Callender has campaigned on diverse issues including the climate crisis, debt cancellation, racial and reparatory justice and LGBTQ+ issues since 2014. He co-founded Kin Cooperative in December 2023 to build a tool that could empower autonomous community mutual aid at the scale needed to take on the economic roots that connect the crises we face today.

Comments

Comments on Lowimpact.org are now closed. To comment or post a query about this topic, please go to the relevant section of the Growing the Commons forum.

1 Comment

This is very educative and informative