This is Part 2 of an interview with Tom Woodroof, who made the move from the world of nuclear physics to the world of mutual credit and monetary change. Part 1 is here. Here I’m going to find out more about his work, and how it can contribute to (quite revolutionary) change. Some readers will begin to see the extraordinary potential of these ideas, I think.

What’s the plan? I know there’s a range of tools that you’re using. You say mutual credit and associated ideas – what are those ideas? What tools are you building and using, and how do they work?

I’ll start with the tools, then move on to the plan. We started with mutual credit (the clue’s in the name).

We discovered Tomaž Fleischman’s work, using another tool called ‘multilateral obligation setoff (MOS)’ in Slovenia. There’s a 2-minute video that explains it. We wanted to introduce the mutual credit idea with minimal disruption to existing circumstances for small businesses, and making minimal demands on people’s understanding of money and finance. It’s an even thinner wedge to go into communities with.And as well as this, we have Chris Cook’s use-credit obligations, and Matthew Slater’s Credit Commons Protocol too.

I can put links to those things, but MOS is new to me. Can you give us a very quick overview of MOS?

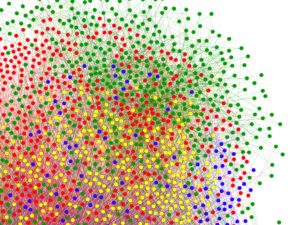

Imagine 100 people in a room, trading with each other. If they only trade with other people in the room, it’s a closed system. If they trade a lot, there will be a lot of dense connections between them. Past a certain density, loops are guaranteed to exist.

Are you talking about existing networks of businesses that trade with each other?

Yes. In Slovenia for example, it’s a developed country with lots of firms exporting, so connections are not so dense. But in Kenya, in the Sarafu network, firms are small and don’t produce for export, so there are extraordinarily dense clusters of trading networks. So different economies have different structures, but even in developed countries, it shouldn’t be too hard to find a set of businesses that do enough local trade, that there will be a density of local connections in which these loops exist.

The simplest loop would be: I owe you money and you owe me money. In that case it’s obvious that we can cancel out some of what we owe each other (for example, if I owe you £10 and you owe me £10 we can call it quits). This still applies if more members join the network, but we can only clear debts if we know the loops exist. This is where MOS comes in. The first thing that has to happen is for the data to be collected. In Slovenia, or in Sardinia, where the Sardex mutual credit network exists, there can be 15-20 businesses trading together, and if they’re not sharing information about trading, they have no way of knowing that these loops exist.

So the first step is to set up a method for collecting data. That’s quite simple. We’ve built an app for the Local Loop project that enables local businesses to submit information about invoices. An algorithm then finds these loops, and clears the maximum amount of debt possible.

What you’re talking about sounds like credit clearing. Why has it been given a fancy name?

Clearing is a more generic term. There are many different ways of doing it, and some say that clearing is only working out what your net position is, but not actually settling. Others say that clearing also includes settlement – where you make the payments to clear everyone’s debts (or as many of them as possible). Credit clearing is shorthand. Everyone knows what it means, but it’s not precise enough. Whereas MOS is a very particular process, where there should be no ambiguity about what you’re talking about.

So do people make a payment to bring their account back to zero after certain time periods?

No. All you do is collect certain information from people’s invoices, then retroactively find loops within the network, therefore reducing the amount of money they need to pay off. It’s not actually introducing any means of payment as such (unlike mutual credit, which is a way for communities to create an internal credit unit that can act as a kind of currency. MOS doesn’t provide this payment system, but it’s a very good stepping stone).

So it just works with existing trading networks. It could just be a massive network of businesses, and the algorithm does the work?

Yes. This is why it’s a nice place to start. With mutual credit, a high degree of trust is required, which means that groups have to remain pretty small. With MOS, because no-one is actually extending each other any additional credit, all members need to do is provide a limited amount of data to a service provider, who then runs the algorithm. This has been done at the national scale in Slovenia, with tens of thousands of participants. You don’t need high levels of trust, because there’s not much risk. But once people have got used to collaborating when it comes to finances, they can be introduced to mutual credit, where the benefits are greater. So these collaborative tools can be layered on top of each other.

So, does introducing mutual credit mean businesses not bringing their accounts back to zero, but having credit limits instead?

These were the kinds of conversations we were having early on in the Mutual Credit Services collaboration, when we developed the trade credit clubs model – another tool in the box that I have to tell you about. We didn’t want to initially present mutual credit as creating a new currency, which can sound quite scary – but just the idea that if we maintain a shared ledger (another type of clearing), then at the end of each month, when all payments and receipts are tallied up, each business can make a single payment that is much lower than the total of their transactions. You’ve effectively cancelled some of your buying against some of your selling. Then you can go a step further, and say that you don’t have to bring accounts back to zero, it would allow them to roll over, within mutually-agreed limits. At that point, you’ve effectively created an internal currency, almost by stealth.

Without having to explain anything about mutual credit?

Yes. So these tools can be implemented, step-by-step, from a MOS network, to trade credit club, to mutual credit club, with obvious benefits at each step, but requiring a bit more trust and collaboration. But at no point do you say to people: ‘ok, you’re going to be creating your own money now.’

So the main effect of all this is that it saves small businesses money?

Yes. It has striking effects on late payments too. Tomaž talks about this a lot. Although easing cash flow issues is an immediate benefit of MOS, in the longer term, you also resolve payment bottlenecks – where a business can’t pay because it hasn’t been paid itself – a bit like unblocking a drain. The MOS algorithm resolves these gridlocks. We know that late payment is a major cause of small business failure. MOS and other mutual credit tools solve these problems, save small businesses and result in better relationships with suppliers. These social benefits are enormous. Small businesses can find new customers and suppliers, and get more favourable terms; and in fact we’re building a directory for the Local Loop project, to help achieve just that.

I’m aware that many people may be a bit bewildered by these new ideas and terminology, but I’ll get more information from you later to create new topics for the Lowimpact site, where we introduce concepts with definitions, benefits and what people can do. I hope to make these ideas as clear and accessible as possible. Any more tools in the toolbox?

Yes, there’s Chris Cook’s use-credit obligations (UCO) idea.

We’ve added that one to Lowimpact already. See here.

And there’s Matthew Slater’s Credit Commons Protocol. So those are the tools we’re working with, and we’re building platforms to bring them to life for people. We use a co-design process, working with partners on the ground to understand what they need, rather than turning up with some tech, without understanding people’s needs first. So co-design is another tool, and finally commons governance, so that everything is owned by the members, as mutuals. So there are social tools that go alongside the economic tools.

What have you achieved so far?

At the moment we have a few projects at various stages of development. The idea is to provide proof of concept. We then find people who see the potential for these tools in their communities, and work with them to build something that works for them.

Is it difficult to find these people?

Yes and no. We’ve got good at explaining the ideas to people at events, or who find us, or even socially, and people get it, although they struggle to explain them to someone else. People can see the potential, but that’s a long way from being ready to build something. We’ve been approached by lots of people, some of whom we’re now working with. Some of them came via Lowimpact.

I’m determined to explain these ideas for a wider audience.

Good.

Where are these pilot projects?

Local Loop in Lancaster is our most advanced project – a MOS network. It’s relatively isolated, with a strong local economy; and it’s the kind of place where people care about their local community. The council and local Chamber of Commerce are receptive too, so we’ve gained traction there quite quickly. We’re launching a trial soon, we’re developing an app, and we have a website with an explainer video.

The point of each of our projects is that they demonstrate one of our tools. In Sweden there’s a project with a business barter network. We’re working with students at a Swedish university to redesign their business barter software using the Credit Commons Protocol. In India we’re working on what will effectively be a High Street Voucher system, which makes use of a small-scale version of use-credit obligations (UCO), which enables consumers to invest in their local high street by giving cash up front to local retailers, in return for discount vouchers. Retailers get cash up front, and consumers get a discount on local spending. In London, we’re building a community-based implementation of mutual credit; and we’ve got a number of other projects in the pipeline.

So to reiterate, we’re working out how to build systems based on use-credit obligations, mutual credit, and the Credit Commons Protocol, in different economic sectors and in different cultural contexts, that are all ultimately interoperable. I imagine more and more of the economy making use of these tools that we’ve got.

So to summarise, you’ve got a toolbox full of alternative monetary and financial tools for trade and exchange, savings and investment, business networks, but also including consumers in those networks too. It’s a bit of a stretch to explain everything in an interview like this, but I want to collect them all together by interviewing you, Dil, Matthew and Chris, and presenting the information in an accessible way on Lowimpact – and to show that they’re part of a package of new ideas that are emerging that can build an entirely new economy. What potential do you think there is for wide-ranging, radical change?

I wouldn’t be working on this if I didn’t believe that there was huge potential, but I don’t want to make any extravagant claims at this point. I am interested in doing academic studies on the potential emergent outcomes of these ideas. What kind of economy would emerge if large numbers of people started adopting these tools? I want to see more solid evidence. So I’m looking forward to collecting data from our projects that we can analyse.

How will the projects be funded in the longer term? Transaction or membership fees?

Something like that, yes. We’re aiming for all our projects to become self-sufficient in a relatively short time period. Each network will have what we call a service member, providing support services to the network, and making a living from doing so. According to fairly conservative projections for membership in Lancaster, we think that the network will become self-sufficient in terms of revenue generated in just over a year. For MCS, we hope to build a range of networks, and charge very small transaction fees for transactions via the Credit Commons Protocol, which will pay for our research, development and support. But first we have to build community-scale projects and show that they work.

Are you looking for more people and more groups to start new projects?

Always.

What kinds of people and organisations?

People who are interested in the work we’re doing, but who are also very practical. The kinds of people we’ve found we can work best with are people who understand their own local economic context, and are deeply embedded in their communities – and who understand what probably will and won’t work in their community. Some work is technical and economic, but most of the work is social. Having said that, we’re interested in talking to people with coding skills. But we’d probably find a use for most skills, one way or another.

I think for the right people, this would be a great project to become involved with.

We’re trying to become a social franchise. Instead of trying to start a business from scratch, people can start a franchise of a model that’s been shown to work. We’ll be wanting to roll out the model nationally and internationally. We can train people and provide the tools to allow them to start a project in their own community, and to plug into a wider network using the Credit Commons Protocol.

What do you think will be your biggest barriers, and how might you overcome them?

In the near term, lack of technical capacity, and core team members . We’d love people to join us, to volunteer with us with a view to paid employment in the longer term.

So you’re looking for volunteers and radical millionaires.

That would be nice, yes.

I think most people intuitively like these kinds of ideas – surprisingly on both sides of the political spectrum – which isn’t something you can say about a lot of things. I think that’s possibly because they’re about removing banks and interest from the equation, which keeps the left happy, but the solutions don’t involve the state – which keeps the right happy. I sometimes hear opposition from people – purists, maybe you could call them – who say ‘I still don’t like it because it’s still about trading, and a market, and I prefer the idea of a gift economy, where we all look after each other without any kind of money or accounting’. I think that’s a lovely idea, but I’ve never heard a coherent plan about how it would work, and can’t see any way we could get there in one step from where we are now. I feel that the mutual credit / use-credit obligations family of ideas represents something much better than we’ve got now, and also a stepping stone for the kind of world those people would like to see, if it’s possible at all. What do you think?

I completely agree. There have to be small stepping stones towards the kind of economy we’d like to see, but which don’t demand that people make huge sacrifices or unfeasible changes to the way they live.

Who else should I interview?

I think it would be interesting to talk to Tomaž, to talk about multilateral obligation set-off. He’s written peer-reviewed papers on it, and he has 20+ years’ experience in running these systems in Slovenia, and studying the effects they could have in combination with mutual credit. Hans-Florian Hoyer as well. I think he’s a retired banker, and he studies the history of these moneyless systems. He talks about something called scontration – a predecessor to MOS, developed in medieval European market fairs.

You mean where they round up at the end of the fair and clear a lot of the debts that people owe each other?

Exactly. They were finding loops without an algorithm to do it. Traders would write down what they’d bought and sold from each other, on account, and at the end of the fair, these specialised accountants would gather everyone’s books, first to find bilateral relationships, then loops, for ways to cancel out debts. Talk to Hans-Florian about the history of these mechanisms – how they originated among medieval merchants, but came to be exclusively used by the financial sector. I think that would be a very interesting conversation. In effect, MCS is about taking these mechanisms back into the real economy.

Right – if it’s good enough for the banks it’s good enough for us. I think these ideas around mutual credit and use-credit obligations are revolutionary. If we can get this snowball rolling, it really does start to change everything.

And I think the further we get with it, the wider the range of people we’re going to be able to work with. Once we’ve got models up and working, and we can prove the benefits, we’re going to have people queueing up saying that they want one in their community.

Looking forward to hearing more about what you achieve. Speak soon.

Cheers Dave.

Highlights

- The point of each of our projects is that they demonstrate one of our tools. These tools can be implemented, step-by-step, from a MOS network, to trade credit club, to mutual credit club, with obvious benefits at each step, but requiring a bit more trust and collaboration.

- We’re working out how to build systems based on use-credit obligations, mutual credit, and the Credit Commons Protocol, in different economic sectors and in different cultural contexts, that are all ultimately interoperable. I imagine more and more of the economy making use of these tools that we’ve got.

- I am interested in doing academic studies on the potential emergent outcomes of these ideas. What kind of economy would emerge if large numbers of people started adopting these tools? I want to see more solid evidence.

- Instead of trying to start a business from scratch, people can start a franchise of a model that’s been shown to work. We’ll be wanting to roll out the model nationally and internationally. We can train people and provide the tools to allow them to start a project in their own community, and to plug into a wider network using the Credit Commons Protocol.